Definition of Option Gamma

The Gamma of an option measures the rate of change of the option delta. Its' number is denoted relative to a one point move in the underlying asset. For example, if the gamma for an option shows 0.015 with a delta of 0.45 then a full point move in the stock (i.e. 35 to 36) means the delta will move to 0.465.

Gamma is calculated via an option model such as Black and Scholes or Binomial. The value is the same for both call and put options.

The Gamma of an option is important to know because the delta of an option is not constant; the delta increases and decreases as the underlying moves. Because delta is essentially our position value in the underlying, the gamma therefore tells traders how fast their position will increase or decrease in value vs movements in the underlying asset.

In other words, Gamma shows how volatile an option is relative to movements in the underlying asset. So, watching your gamma will let you know how large your delta (position risk) changes.

When is Option Gamma Highest?

Gamma is not linear. Like Delta, Gamma has curvature and is effected by the inputs that calculate the Gamma, the most notable forces that influence it are factors such as the difference between the strike price and the underlying price, the time to expiration of the option and the implied volatility used in the model. Interest rates and dividends are also factors that effect the value of the Gamma, however, the magnitude of these inputs is minimal when compared to the previously mentioned variables.

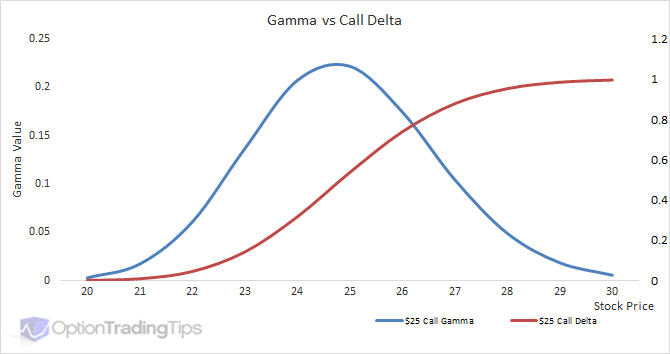

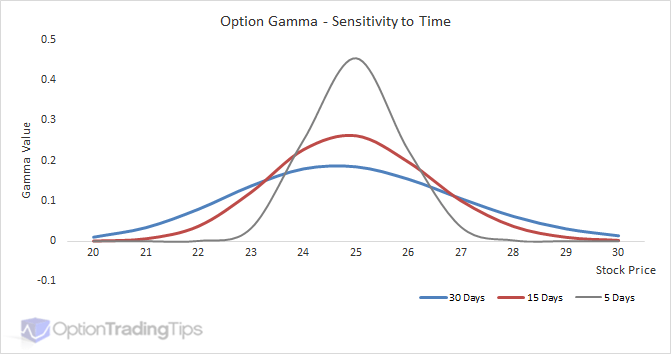

The attention on a Gamma's sensitivity is mostly focused on its' position relative to the underlying price. Looking at the above graph you can see that the Gamma reaches its' peak when the option is at-the-money and tapers off either side. When an option position moves towards the ATM level, the changes in the position delta, and hence the position value relative to the stock, change with greater amounts. Options that are either deep ITM or deep OTM experience less variability as the stock price changes and therefore will show low Gamma values.

Time and Volatility

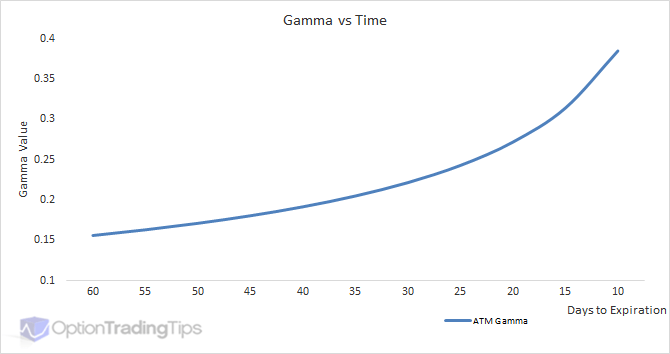

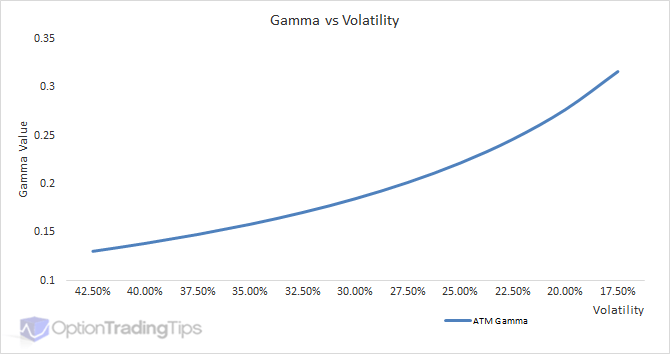

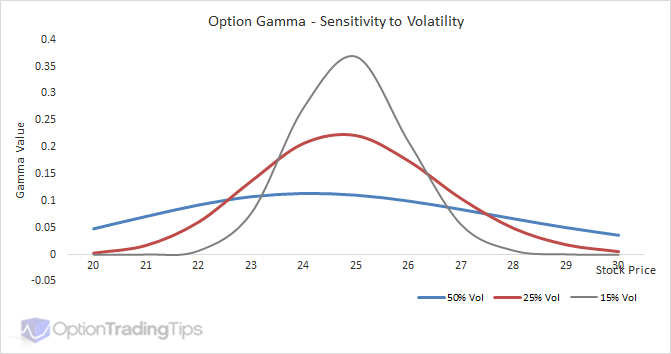

Adding more time to an option contract increases the likelihood of that option expiring in-the-money. Because higher volatility also increases the chances of an option's in-the-moneyness, both volatility and time have the same effect on an option's Gamma value.

The above graphs show how increasing time/volatility value reduces the Gamma of the option and hence it's sensitivity to changes in stock price.

While adding more time to an option increases the VAUE of the option, it generally reduces the option's Gamma. With more time to expiration the option becomes less sensitive to movements in the underlying asset. However, as the option approaches its' maturity date, its' time value will move towards zero and then become more responsive to changes in the underlying price.

These graphs provide a great way to look at how Gamma is effected by the passage of time. Both plot a $25 call option's Gamma across a range of underlying prices, however, on each graph is shown 3 different times to maturity. This is so you can see how the Gamma value becomes the highest when it is both ATM and close to expiration. When this happens, option positions will have the highest fluctuations in position value (Delta).

What is Long Gamma?

Note: The Gamma value is the same for calls as for puts. If you are long a call or a put, the gamma will be a positive number. If you are short a call or a put, the gamma will be a negative number.

When you are "long gamma", your position will become "longer" as the price of the underlying asset increases and "shorter" as the underlying price decreases.

Conversely, if you sell options, and are therefore "short gamma", your position will become shorter as the underlying price increases and longer as the underlying decreases.

This is an important distinction to make between being long or short options - both calls and puts. That is, when you are long an option (long gamma) you want the market to move. As the underlying price increases, you become longer, which reinforces your newly long position.

If being "long gamma" means you want movements in the underlying asset, then being "short gamma" means that you do not want the price of the underlying asset to move.

A short gamma position will become shorter as the price of the underlying asset increases. As the market rallies, you are effectively selling more and more of the underlying asset as the delta becomes more negative.

Gamma in Option Chain

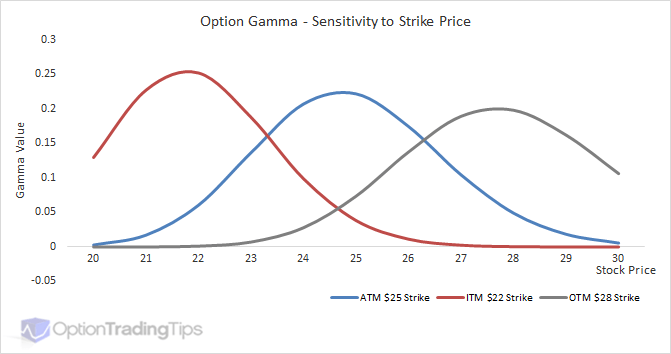

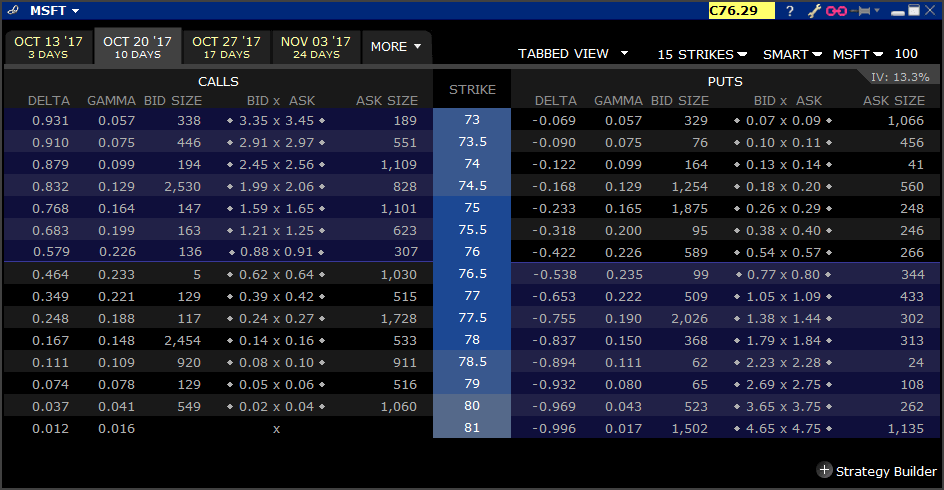

The graphs shown here, display gamma with constant volatility and strike price. In practice, options across different strike prices have different implied volatilities and therefore a different gamma distribution.

The above is an example of what Gamma and Delta values look in practice. This is an option chain of MSFT stock options showing an expiration 10 days out.

Notice how the ATM strike of $76.50 shows the highest Gamma value of 0.233 for the calls and 0.235 for the puts. I'm not sure why they are different here...they really should show exactly the same value for the call and the put - perhaps a rounding issue. Nevertheless, 0.002 difference is fairly immaterial.

If the stock trades up 1 full point to $77.29 then the $76.50 call option Delta will move from 0.464 to 0.697. So while the stock price has only moved 1.3% your effective position in the underlying has increased by 50%.

Black Scholes Gamma

If you're interested in knowing how to calculate option gamma in excel, you can download my option pricing spreadsheet for a working example. Otherwise, here are some code examples:

Excel VBA

Option Gamma Formula

NdOne(UnderlyingPrice, ExercisePrice, Time, Interest, Volatility, Dividend) / (UnderlyingPrice * (Volatility * Sqr(Time)))Where:

NdOne = Exp(-(dOne(UnderlyingPrice, ExercisePrice, Time, Interest, Volatility, Dividend) ^ 2) / 2) / (Sqr(2 * 3.14159265358979)) dOne = (Log(UnderlyingPrice / ExercisePrice) + (Interest - Dividend + 0.5 * Volatility ^ 2) * Time) / (Volatility * (Sqr(Time)))

29 Comments

Arwen July 17th, 2014 at 1:30am

Thanks again,Peter!

Your explanation is very clear :-)

Peter July 17th, 2014 at 12:52am

Hi Arwen,

When your position is "long gamma" it means that upward movements in the underlying price increase your delta (longer). Conversely, downward movements in the base price reduce your position delta (shorter).

In the above, as the market rallies and your position becomes longer in delta you must sell the underlying to remain delta neutral. As the market begins to sell off, you then become shorter requiring you to buy back deltas.

So, as the market rallies, you're selling into it - when it falls you're buying it back. If this is done in large quantities it can have the effect of restricting the movement of the stock.

The reverse is true for short gamma; as the market rallies, your position delta becomes shorter and you'll need to hedge by buying stock. In this case you're buying as the market rallies to square up your delta and selling as the market falls.

Does that explanation help?

Arwen July 16th, 2014 at 2:38am

Hello Peter,

I have a question on relationship between "keeping delta-neutral position" and "volatility movements".

If the market participant wants to keep delta-neutral position (net positive gamma) by the action of buying and selling large number of stock, then this dampens volatility.

If the market participant wants to keep delta-neutral position (net negative gamma) by the action of buying and selling large number of stock, then this increases volatility.

I am not very clear about the relationship behind them. Could you please give some explanation? Thank you very much!!

Arwen July 13th, 2014 at 2:28am

Thanks, Peter!

Now, I understand that, from a seller's point of view, the short position is worthless.

Peter July 12th, 2014 at 4:45am

Hi Arwen,

When you buy an option you pay the premium (option price) to the option seller; so as the option seller you receive the premium at the time of trade.

With a short position, you want the price of the option to decrease, ideally to zero, at which point the option will be worthless. Once the option expires worthless, you, the option seller have benefited by retaining the premium received by the buyer of the option.

If the price of the option increases, you may end up buying the option back (to square of your short position) at a higher price than what you sold it for, which means you will make a loss in this situation.

Let me know if anything is still unclear.

Arwen July 12th, 2014 at 2:16am

Hi Peter,

You answered Darryl's question on 4.30.2012.

You said "If you are short the position is still worthless, however, you make a profit - being the premium received for selling the option." I am confused. If the position is short, we can make profit. But why the position is still worthless? How to explain this?

Thank you!!

Peter April 23rd, 2014 at 6:56am

Hi Rawdy,

Short gamma volatility trades typically want volatility and market movements to remain stable so if the market gaps large and you are short gamma and delta neutral you will lose money.

However, you can be short gamma and also short delta i.e. short naked call option. In this case if the market gaps open lower you will most likely be making money in this situation.

rawdy April 20th, 2014 at 3:27am

what if gamma is short and market open gap down will i make loss or profit

Peter April 30th, 2012 at 7:25pm

Hi Darryl,

The Position Delta = Delta x Contract Size x Number of Option Contracts.

In the post by Charlie, he mentioned that the contract size was 10mt (btw, I don't know what mt is, but let's just treat it as some standard unit) with the option delta being -0.2138 on 100 short call options. So, -0.2138 x 10 x 100 = 213.

For your put option question - in both cases, whether you're long or short the option the delta approaches 0 as the underlying price increases. Your long/short position just determines whether your delta will approach 0 from a positive number or a negative number. Also, the concept of ITM/OTM doesn't depend on your long/short position either. If a put has a strike price of 90 and the stock is expires at 100 then the put option is OTM. If you are long at the expiration date your position is worthless and you loss is the premium. If you are short the position is still worthless, however, you make a profit - being the premium received for selling the option.

Let me know if anything is unclear.

darryl April 30th, 2012 at 4:37pm

Hi Peter,

I'm new to the greeks and wanted to pick up on the last comment. Why if delta is -0.2138, why would you buy 213 lots rather than 21?

In addition, 'I.e. for a long put if the underlying price increase from 50 to 60 the delta will go from -0.40 to -0.20 (longer)'. - i undertsand this as the option moves further otm and so delta moves closer to zero.

'For a short put the delta is reversed. So as the underlying price goes from 50 to 60 the short put delta will go from +0.40 to +0.20 (shorter)'. - If i'm short a put and the underlying price increases then doesn't my option move closer to/become more itm, so doesn't my delta increase?

Many thanks

Add a Comment