Option Strategies

Combine calls and puts to construct specific price outcomes. Option strategies give you the flexibility to profit from rising, falling and directionless markets.

Bullish strategies

Profit from a Rising Market

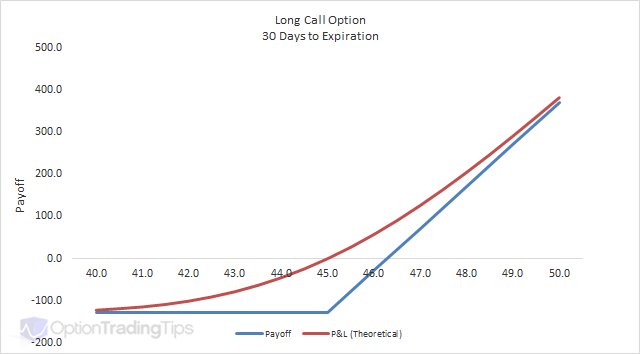

Long Call Option →

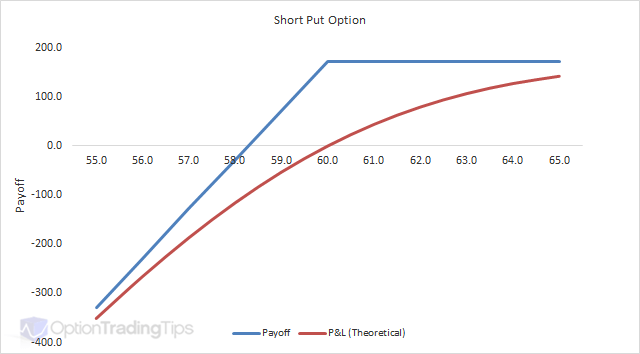

Short Put Option →

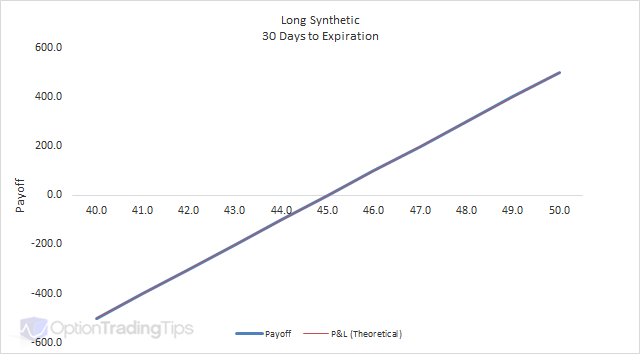

Long Synthetic →

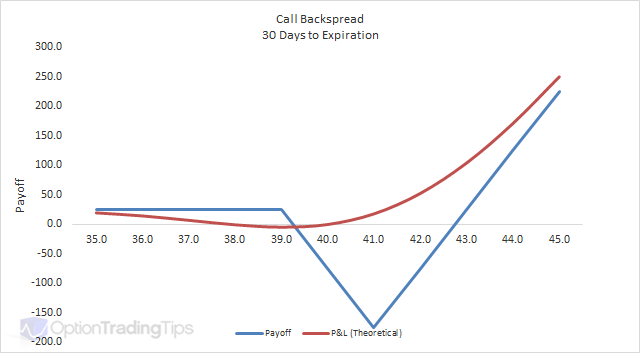

Call Backspread →

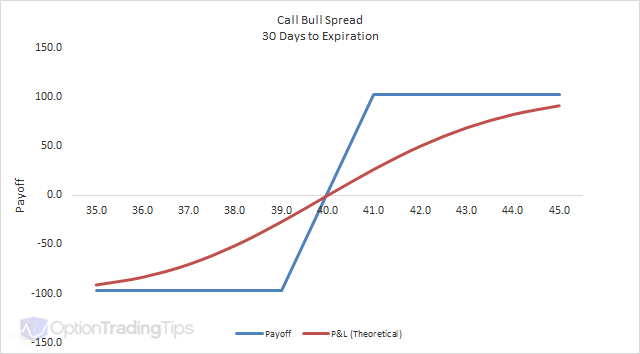

Call Bull Spread →

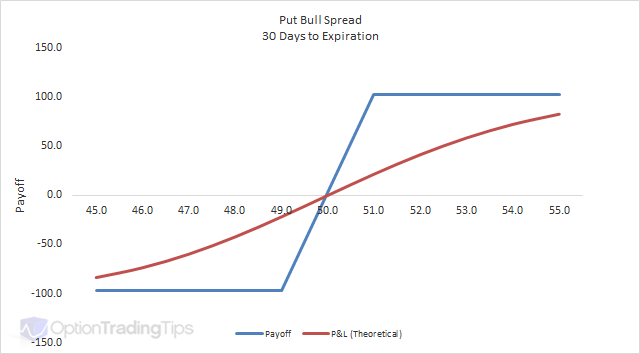

Put Bull Spread →

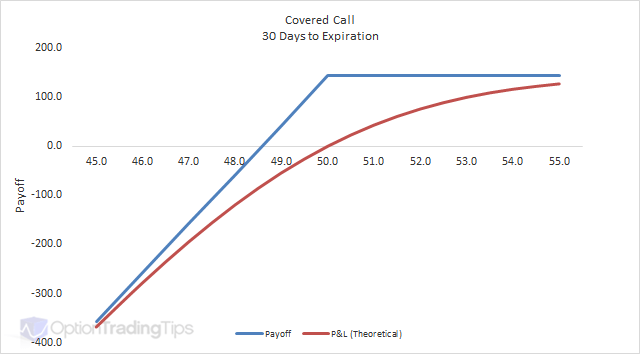

Covered Call →

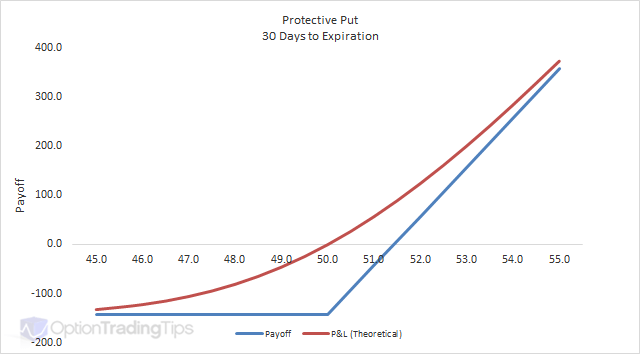

Protective Put →

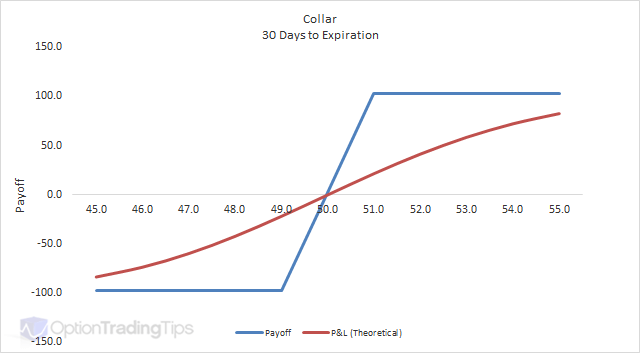

Collar →

Bearish strategies

Profit from a Falling Market

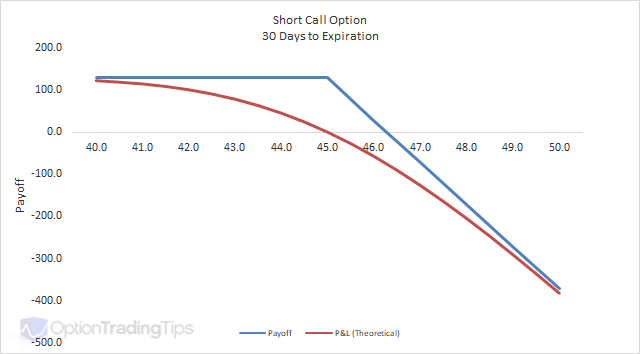

Short Call Option →

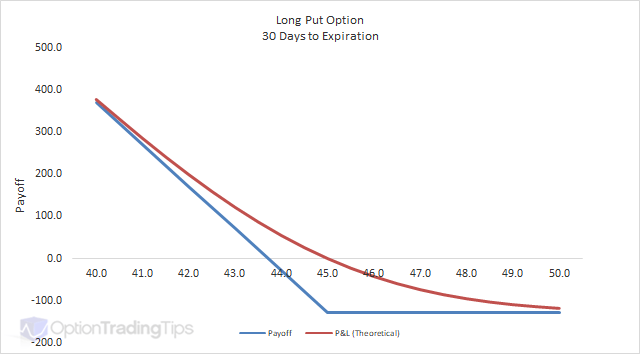

Long Put Option →

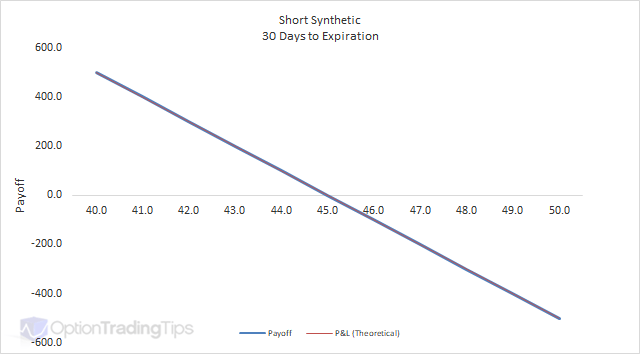

Short Synthetic →

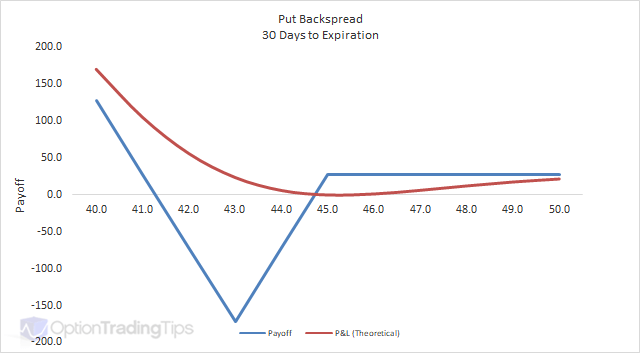

Put Backspread →

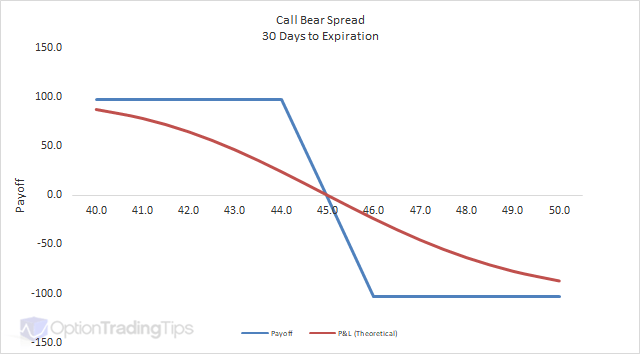

Call Bear Spread →

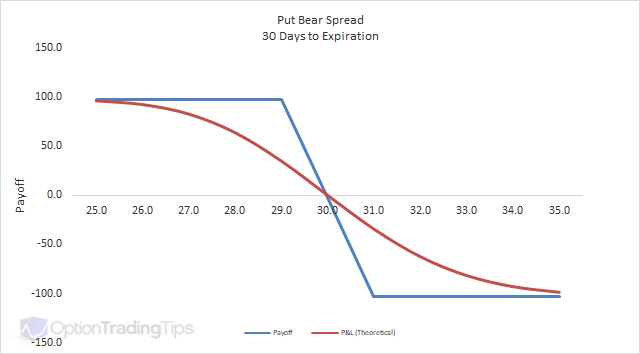

Put Bear Spread →

Market neutral strategies

Profit in a Sideways Market

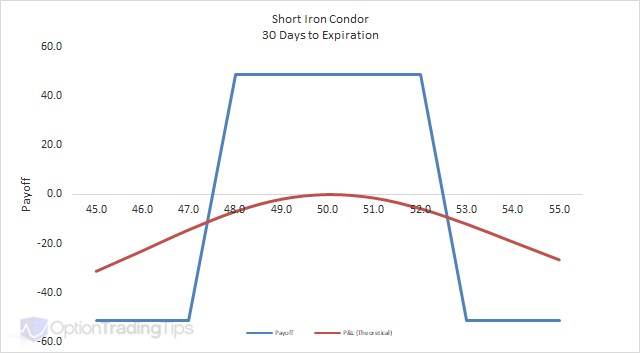

Iron Condor →

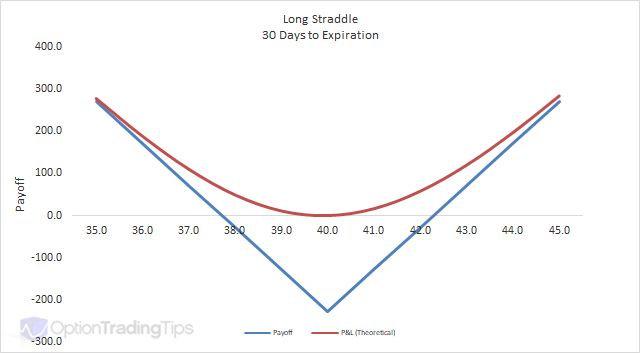

Long Straddle →

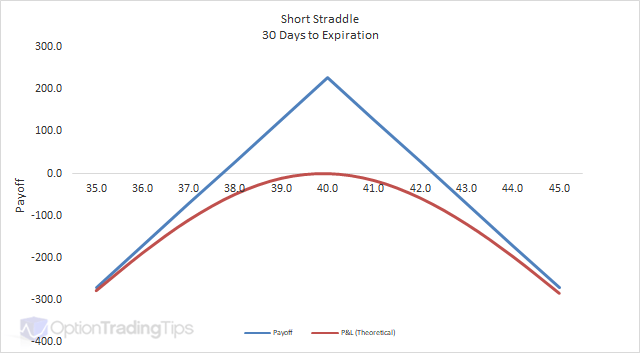

Short Straddle →

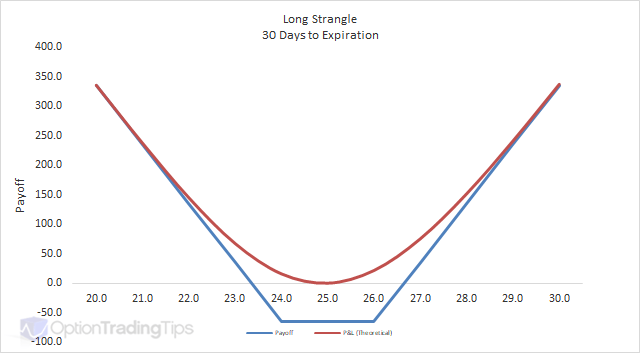

Long Strangle →

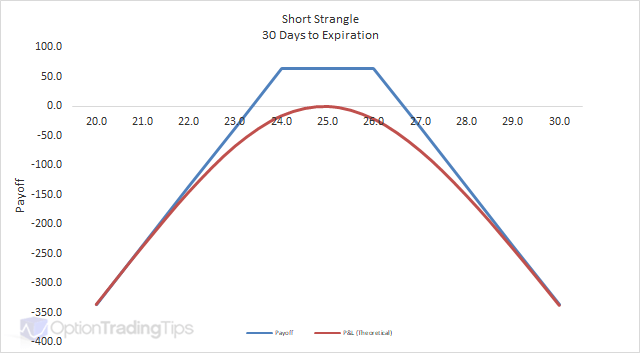

Short Strangle →

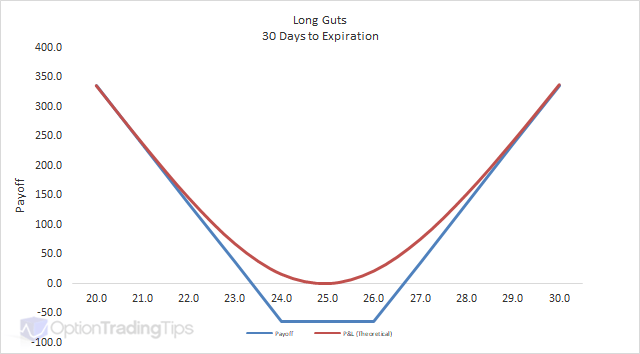

Long Guts →

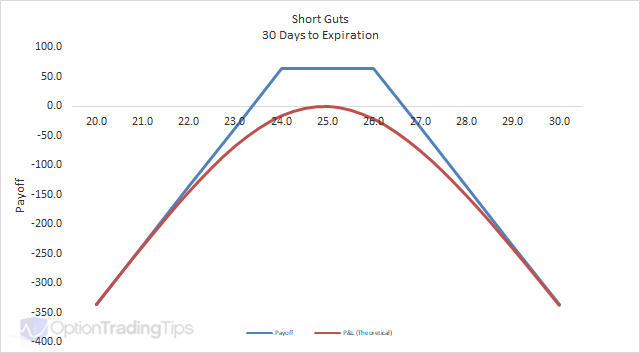

Short Guts →

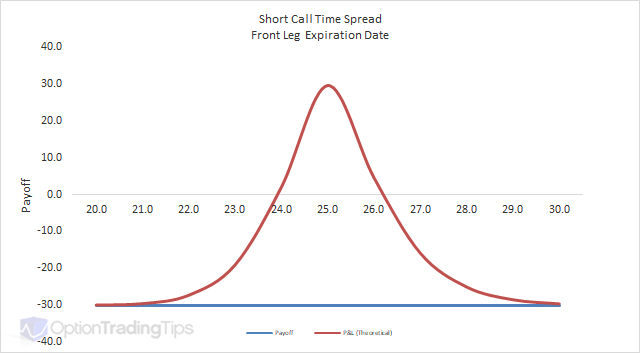

Call Time Spread →

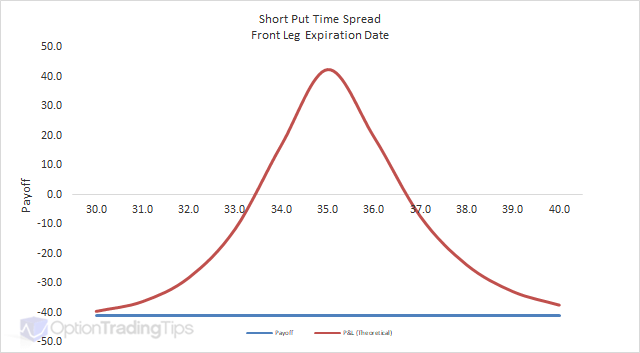

Put Time Spread →

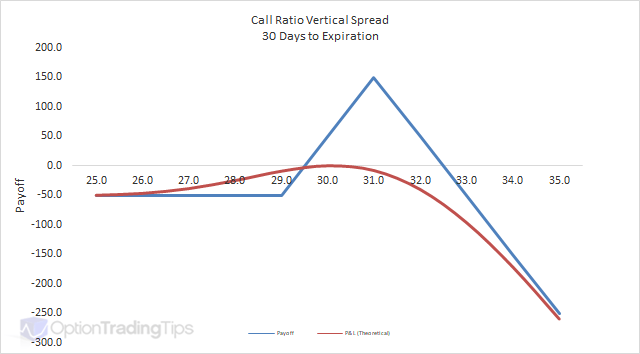

Call Ratio Vertical Spread →

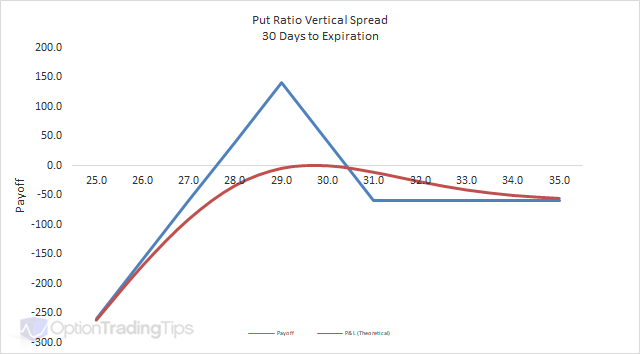

Put Ratio Vertical Spread →

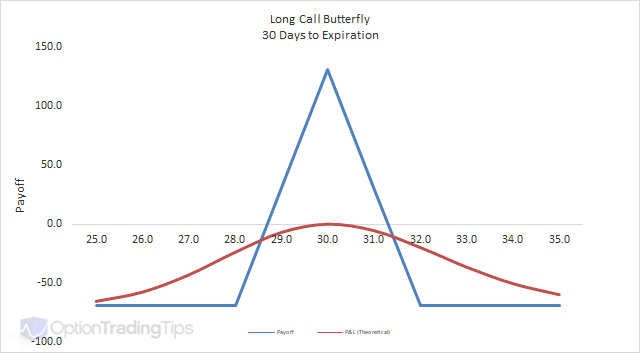

Long Call Butterfly →

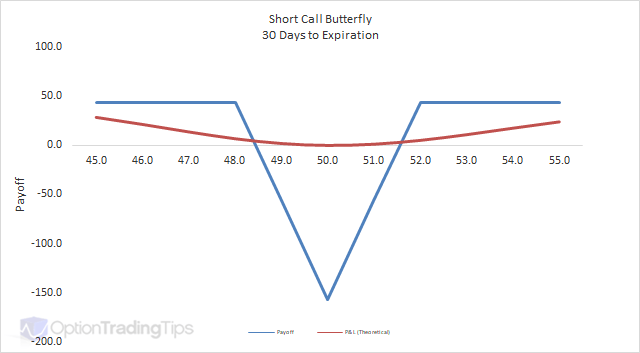

Short Call Butterfly →

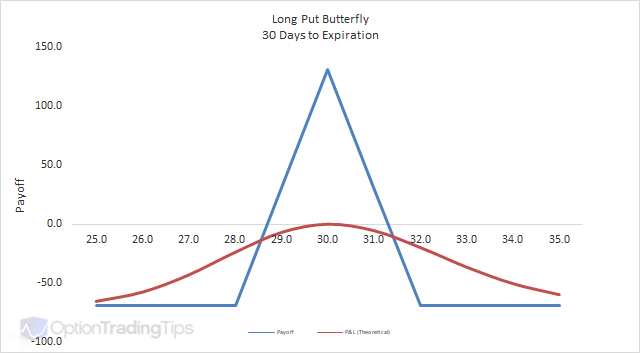

Long Put Butterfly →

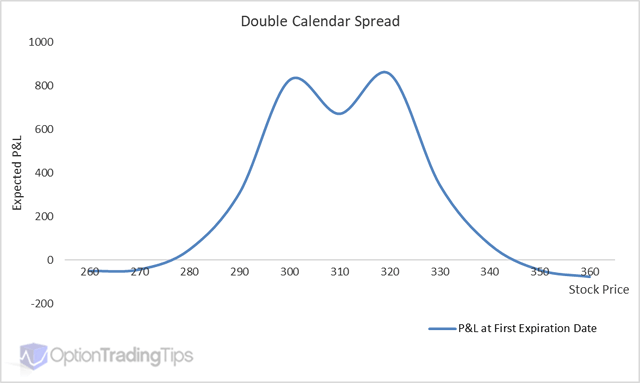

Double Calendar →

About Option Strategies

Generally, an option strategy involves the simultaneous purchase and/or sale of different option contracts, also known as an option combination. There is such a wide variety of option strategies that use multiple legs as their structure, however, even a one legged Long Call Option can be viewed as an option strategy.

But what if you bought a call and a put option at the same strike price in the same expiry month? How could a trader profit from such a scenario? This is called a Long Straddle — one of the most popular market neutral strategies.

In this example, imagine you bought 1 $40 July call option and also bought 1 $40 July put option. With the underlying trading at $40, the call costs $1.14 and the put costs $1.14 also — a total outlay of $228, which is your maximum loss.

If the market rallies, the call option becomes increasingly profitable while the put expires worthless. If the market sells off, the put becomes profitable while the call expires worthless. Either way, as long as the move is large enough to exceed the $228 cost, you profit.

This is just one example of an option combination. There are many different ways to combine option contracts together — and also with the underlying asset — to customise your risk/reward profile.

For further analysis tools, take a look at the Volcone Analyzer — it analyses any option contract and compares it against historical averages, helping you decide whether to buy or sell.

105 Comments

Rakesh March 17th, 2012 at 10:38am

Hi Peter,

I wanted to know the basics which I need to keep in mind before trading in "EXPIRY" ?

When we need to write a CALL/PUT ?

Thx

Peter February 26th, 2012 at 4:44pm

Mmm, that's a tough question to answer here Rakesh ;-) I'd say your best bet would be to invest in a program like MultiCharts . MultiCharts can chart, scan and auto-trade stocks through many different brokers. Plus, it provides an easy to use scripting language that allows you to design and backtest trading ideas before risking real money. I have it and love it!

. MultiCharts can chart, scan and auto-trade stocks through many different brokers. Plus, it provides an easy to use scripting language that allows you to design and backtest trading ideas before risking real money. I have it and love it!

Rakesh February 26th, 2012 at 11:36am

Hi Peter,

What things I need to keep in mind before getting into intraday trading in STOCKS?

I also wanted to know the procedure of picking the right stock in intraday trading?

Thx

Peter February 23rd, 2012 at 5:17pm

Hi Joel,

It depends on what you define as the ATM strike. If you simply say that ATM strike is the strike closest to the stock price, then yes the call will normally have a higher premium than the put. However, the ATM strike should really be driven by the "forward price" of the stock.

As option contracts carry the right to exercise at a point in the future, their value is first based on the future price of the stock, which is the stock price plus the cost to hold the stock (cost of carry or interest rates) less any dividends received during that period.

As you apply the interest rates and dividends to the current stock price you will calculate a price different to the stock and this is the true ATM price. For retail traders who are simply eye balling the option screen to see where the ATM is, just using the stock price is good enough, which is why they've noticed that the call premiums are higher than the puts as the true forward price is actually higher than the stock price.

Call, put and stock prices for the same strike are all related and cannot violate put call parity. Take a look at that link to read more and let me know if I've missed anything or if you have any questions.

Joel H. February 23rd, 2012 at 8:58am

I just finished reading a book on options and one of the discussion points was that an ATM call will always have a higher premium than a put at the same strike. If I find a put which has a higher premium then a call at the same strike price, is this unusual? Is there a way to take advantage of such a situation? Is it fair to assume that this is a temporary situation? Thanks in advance.

Peter February 23rd, 2012 at 2:28am

Hi Ash,

If the option is out-of-the-money then, yes, it will begin to lose value very quickly as expiration approaches. If you are happy with any profit you've made already then you should exit while you can.

Ash February 23rd, 2012 at 1:39am

Hi Peter, I have a question on when to close out my position on a call option. I currently have a April call option and i wanted to know if there are any best practices around when to closeout your position if you are not planning on purchasing the stock at expiry?. I am asking this because as time goes by the price of options go down. It is end of feb now and my options expire in Apr. Your input is appreciated.

Peter February 19th, 2012 at 5:04pm

Hi Rakesh,

If you want limited risk and unlimited profit potential then you are best looking at positions like long call, long put, long straddle, long strangle etc - these are strategies where you are net long options.

Rakesh February 19th, 2012 at 8:59am

Hi,

Can anybody tell me the statergies that I need to keep in mind before trading in "Options"? So that the risk percentage is nominal and the probality of profit is high.

Peter February 12th, 2012 at 5:09pm

Hi eh,

This strategy is called a short guts and is similar to a short strangle except you are shorting a put with a higher strike price, where a strangle sells the put with a lower strike price.

The payoff calculation is a little different also: with a short strangle the max profit achievable is the premium received. But with a short guts the max profit is the net premium received minus the difference between the two strikes, so in this case $5 (multiplied by whatever multiplier the index carries).

Can I ask why would choose this approach instead of selling the 1100 call and the 1050 put?

Add a Comment