Buying a Call Option

| B/S | Strike | Type | Price |

|---|---|---|---|

| Buy 1 | $45 | Call | $1.29 |

| Net Debit | $129 | ||

A long call option gives the buyer the right to buy the underlying asset at the strike price. The option buyer pays a premium for this right to the seller of the option.

The Max Loss will only ever be the premium that is paid up front to buy the option.

The Max Gain is uncapped and will rise with as long as the underlying price rises.

Characteristics

When to use: When you are bullish on market direction and also bullish on market volatility.

A long call option is the simplest way to benefit if you believe that the market will make an upward move and is the most common choice among first time investors.

Being long a call option means that you will benefit if the stock/future rallies, however, your risk is limited on the downside if the market makes a correction.

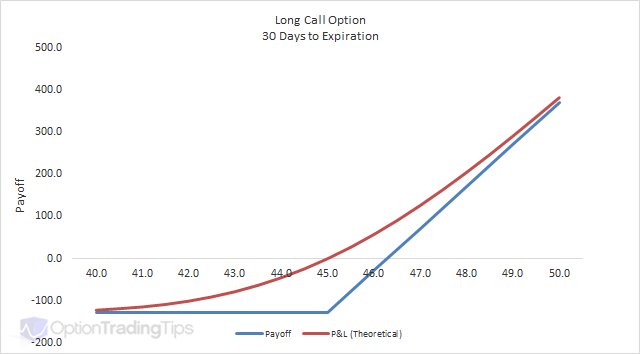

From the above graph you can see that if the stock/future is below the strike price at expiration, your only loss will be the premium paid for the option. Even if the stock goes into liquidation, you will never lose more than the option premium that you paid initially at the trade date.

Not only will your losses be limited on the downside, you will still benefit infinitely if the market stages a strong rally. A long call has unlimited profit potential on the upside.

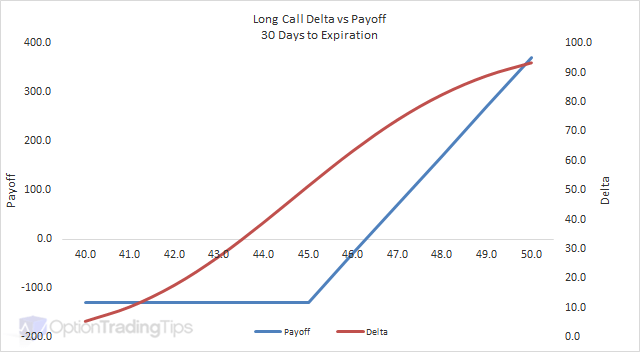

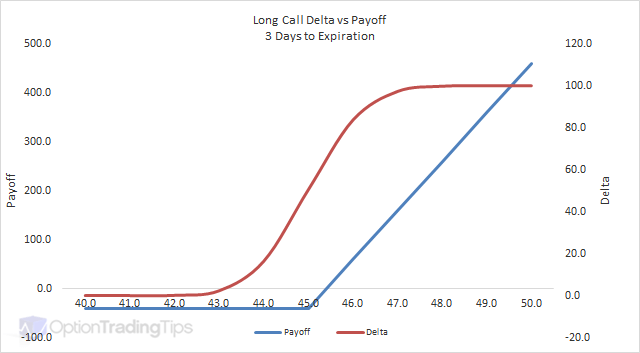

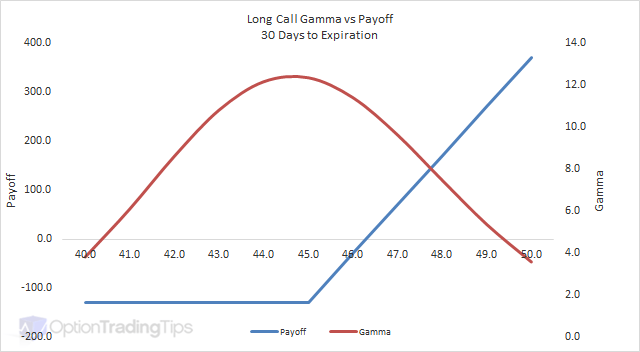

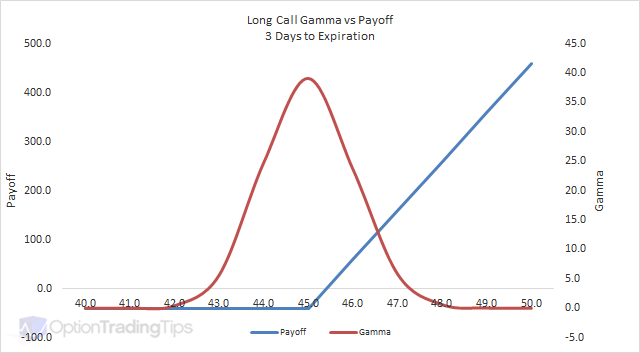

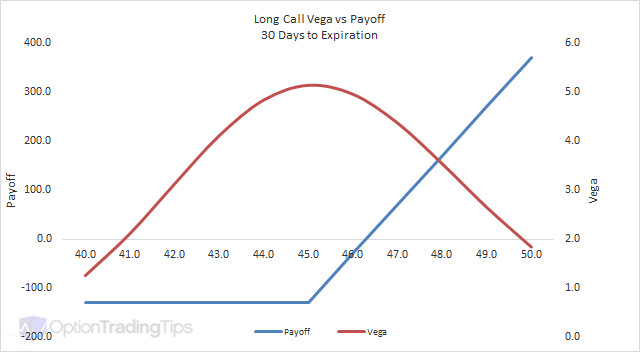

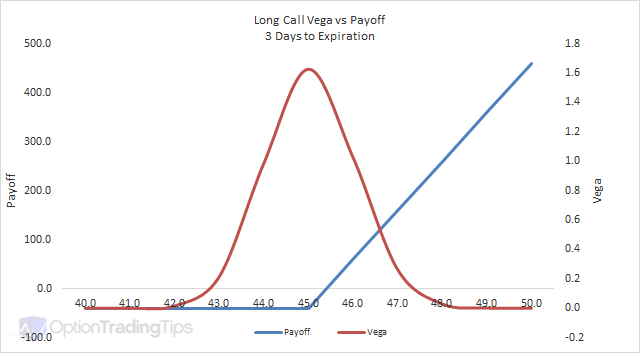

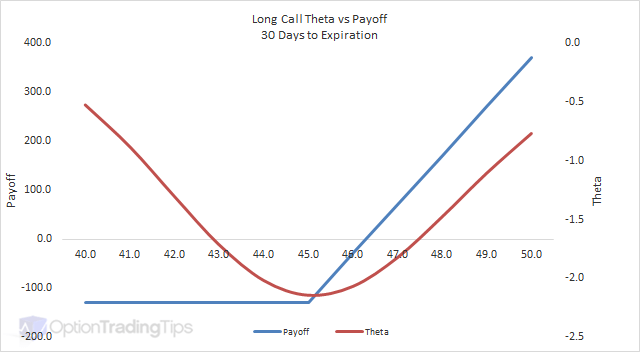

Long Call Greeks

Delta

Gamma

Vega

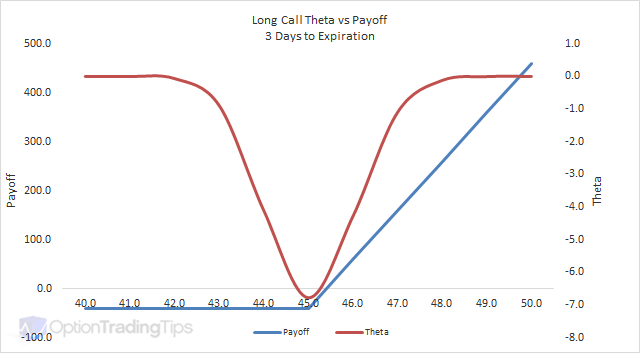

Theta

201 Comments

Peter August 25th, 2011 at 7:33pm

Hi Tom,

Option premiums generally decrease the further they are out of the money. Hence, the cheaper they are to buy. So, your percentage returns are magnified upon a large move. However, the rate of change (i.e. option delta) is lower for out of the money options. If the market does move, out of the money options will not change as fast as in/at the money options.

The decision as to what call option to buy comes down to just how bullish you are on the stock. If your view is only slightly bullish then you would be best off buying an at the money option, however, if you expected the stock to stage a massive rally then you would be better off picking an option in line with the expected price of the stock post rally.

Call options the are in the money (strike price below the stock price) have higher deltas and therefore their prices move more in line with the stock that it is based on. This means that you can take advantage of an upward move in the stock at the same rate as if you owned the stock without making the full purchase.

In your example, buying a $4 strike call option on a stock that is trading at $7 would be worth at least $3 in premium, let's say $3.50. Buying 1 call option contract would cost you $350 (100 shares) and this option's price changes are likely to move in line with the stock. If you were to buy the stock outright this same position would cost you $700.

Tom August 25th, 2011 at 2:39pm

Peter.

Can you please explain to me 2 things.

1)If i am bullish on xyz trading at say 7. I can buy contracts at strike prices of 8, 9, 10, 11 etc. Obviously the lower strike prices carry less risk and should be closer to realization. But how does one choose which to pick - especially since I can trade an option w/o exercsing it, and hence it really doesn't have to hit the strike price. Is there more upside to a further out strike price?

Even more confusing for me is, why are there contracts for calls below the market price? Why can I purchase a strike price of 4 when a stock is at 7? (i mean this is no put contract)Does that mean I could exercise the option anytime (it already hit the strike price since its below the actual value) if for a example a stock got upgraded. Is this this supposed to be some hedge in case the stock looses value?

Milton August 24th, 2011 at 10:37pm

Peter...great stuff...

Nat...get some flash cards

Peter August 7th, 2011 at 7:51pm

Yes - provided that the buyer has a "long" position.

Nat August 7th, 2011 at 7:32pm

Hello Peter,

Thank you very much for your explanation. This means that if I sell my call option to someone to close the position and reap my profit or cut my loss, the person who bought it from me will be guaranteed to buy his share from my original seller, right? (if my original seller has not closed out his position)

Peter August 7th, 2011 at 6:42pm

It's no bother, you're welcome to ask questions.

Think of an option position the same way that you would a stock.

Say you buy 100 shares of stock and then you go and sell 100 shares of stock. After the sale of stock, you no longer have any shares left - your long position of 100 shares has been "offset" by the sale of 100 shares.

I think the confusion you have is that you are imagining a market where there are only a few players - you, a buyer and a seller, where each is trading around the same allotment of contracts.

But in practice the markets are full of buyers and sellers and the process (called novation) of allocating the contracts and positions of each participant is handled by the clearing houses.

Nat August 7th, 2011 at 9:16am

Hello Peter,

I am pretty much clear on the second question. However, for the first one, then what would happen to the buyer of my call option? Who will be obliged to pay him the $10 at the end of the expiry date?

Thank you again and sorry bugging you. I am kind of new to all of this and the only part I don`t get it is offsetting the position.

If you would be so kind to provide a numerical example of how offsetting a position works, I would really appreciate it.

Peter August 7th, 2011 at 8:45am

With your first question I was thinking you were describing something like this;

Bought 1 $10 strike call option

then

Sold 1 $10 strike call option

Now, because you've sold out of the same contract you no longer have a position at all. However, if you did this;

Bought 1 $10 strike call option

and then

Sold 2 $10 strike call options

In this case, because you are now selling more contracts then you are holding you would net be short 1 $10 strike call option.

And yes, for your second question, if you had of sold the call option instead and the stock ended up at $11 then you would have made the $1 profit instead of the loss.

Nat August 7th, 2011 at 8:00am

Hello Peter,

Thank you so much for your quick response. I just have a couple more questions if you could kindly clarify it for me.

According to my first question, I don`t understand why I will no longer have an option position if I sell my call option because I have turned into the seller of the call option. Won`t I have the obligation to sell the share to the person whom I sold the call option as the seller?

Secondly, in the second case where I would have made a loss of $1, would it have been better if I had sold my call option contract because it would have been worth a little more since the price of the share is higher to offset the position instead of exercising it?

Peter August 7th, 2011 at 7:42am

Hi Nat,

For your first question, if you offset the bought option by selling the same option in the same quantity then you no longer have an option position.

You would only have to worry about the option being exercised if you were "short" an option - i.e. selling an option without first buying an option.

And yes for your second question - you will make a $1 loss if the stock is only at $11 at the expiration date.

Add a Comment