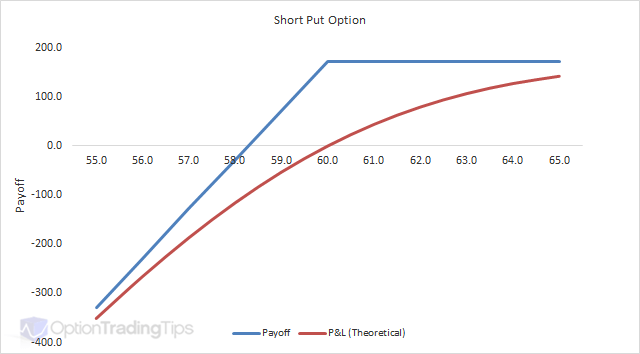

Short Put Option

| B/S | Strike | Type | Price |

|---|---|---|---|

| Sell 1 | $60 | Put | $1.72 |

| Net Credit | ($172) | ||

A short put is the sale of a put option. It is also referred to as a naked put.

Shorting a put option means you sell the right to buy the stock. In other words you have the obligation to buy the stock at the strike price if the option is exercised by the put option buyer.

The Max Loss is unlimited in a falling market, although in practice is really limited to the total value of the exercised stock position — as a stock cannot trade below zero.

The Max Gain is limited to the premium received for selling the put option.

Characteristics

When to use: When you are bullish on market direction and bearish on market volatility.

Like the Short Call Option, selling naked puts can be a very risky strategy as your losses can be significant in a falling market.

Although selling puts carries the potential for large losses on the downside they are a great way to position yourself to buy stock when it becomes "cheap". Selling a put option is another way of saying "I would buy this stock for [strike] price if it were to trade there by [expiration] date."

A short put locks in the purchase price of a stock at the strike price. Plus you will keep any premium received as a result of the trade.

For example, say AAPL is trading at $98.25. You want to buy this stock but think it could come off a bit in the next couple of weeks. You say to yourself "if AAPL sells off to $90 in two weeks I will buy."

At the time of writing this the $90 November put option (Nov 21) is trading at $2.37. You sell the put option and receive $237 for the trade and have now locked in a purchase price of $90 if AAPL trades that low in the 10 or so days until expiration. Plus you get to keep the $237 no matter what.

The risk here is that the stock tanks before the expiration date leaving you with the potential to be exercised and take delivery of the stock at $90 when it, say, is trading at $80 when you are assigned the stock.

If the drop occurs early, and it is significant i.e. at or below the strike, you would want to re-evaluate your trade and potentially exit the option position before the losses increase. If the drop in stock value occurs close to the expiration date and is not yet through the strike price, a good exit plan is to put a short stop order on the stock itself. That way you'll be covered on the exercise if it happens while leaving the option position open to capture the remaining time value.

Option Strategy Swipe File

Ditch the text books. Instantly choose the right strategy for your needs with my one-page strategy template guide.

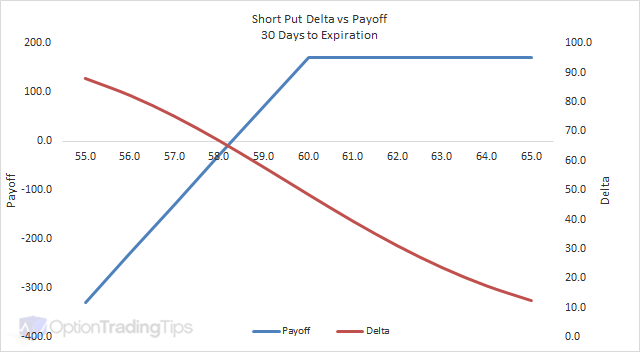

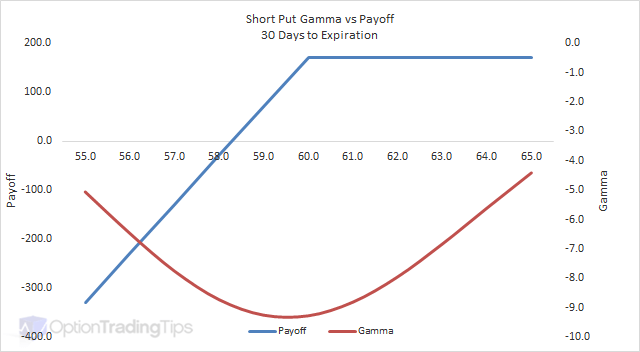

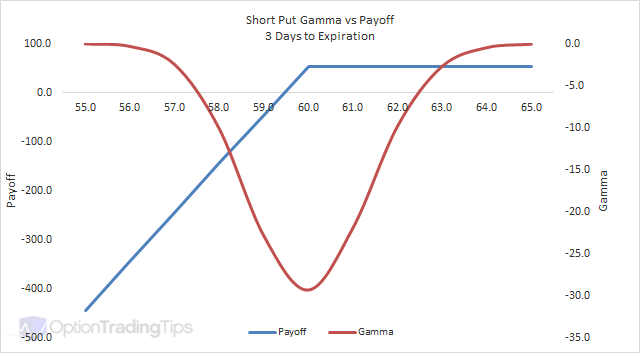

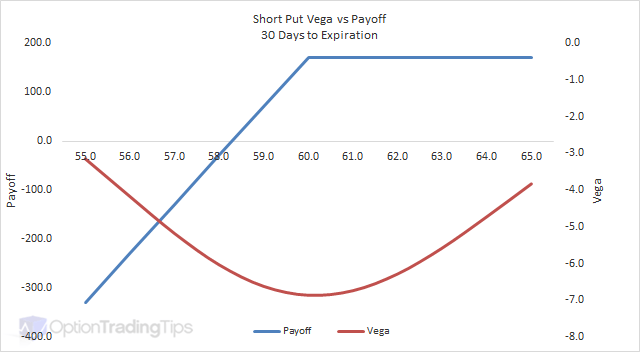

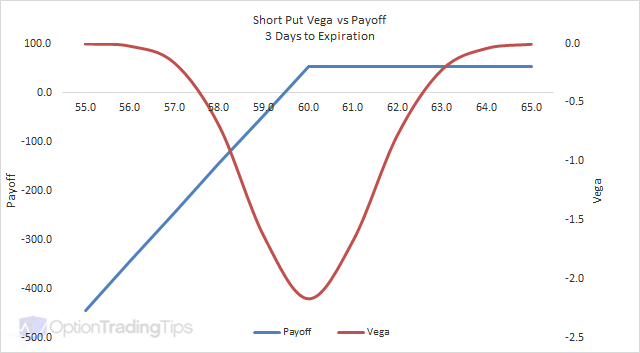

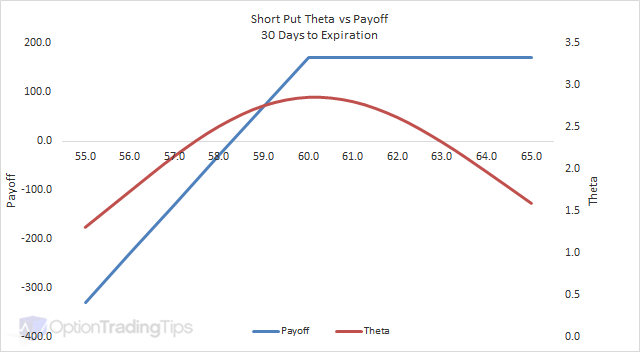

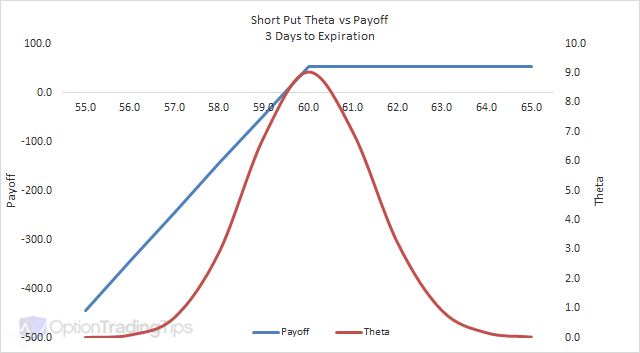

Short Put Greeks

Delta

Gamma

Vega

Theta

56 Comments

Pk February 16th, 2015 at 8:16pm

Peter,

I just came across this article today, don't know if you still get messages from it...

I'm kinda new to options and trying to learn.

In your last response to Francois, you said that the risk is that if the stock rallies, you are left with only the short position.

But what if we did the final part in Francois's suggestion and placed a stop order to sell if the stock recovers above 89?

Thanks.

Francois April 28th, 2014 at 7:02am

Hi Francois,

Nice, I like your thoughts on this, thanks for posting!

I think one problem is that you aren't guaranteed to be assigned long stock by selling the $90 put, but if the stock does go to $89 and you have a short stop order - that you will be filled on. So, if the stock does drop to $89 then you have upside risk; you're short the put sure, but if the market rallies prior to expiration you will only have a short stock position.

Francois April 26th, 2014 at 10:25am

Protecting 'naked' positions when the market moves against you.

Why not simply add a stock position (place stop order at same time you enter naked put or call) to your naked positions when they get ITM?

IE: XYZ trading at $100

- SELL 90PUT for $2 (break-even is now $88, max profit $2, max loss $88)

- Place stop order to SHORT stock at, say, $89

- IF stock goes down below $89 then you are entered SHORT on XYZ @ $89 so that you then get to keep $1 of your premium sold AND you are fully protected as the stock continues to decline

- From there you can place stop order to sell stock if price recovers above $89, etc.

If at expiry XYZ declined to $80:

- you have the $2 premium on the 90PUT sold

- you get assigned the stock at $90 (pay $90 minus $2 credit received but it's worth $80 so loss of $8)

- you cover your short position (sold for $89, buy back at $80 = profit of $9)

- overall profit of $1

Same goes for selling naked calls; place stop order slightly ITM to enter LONG stock and you get to keep some of your premium sold AND fully protected as stock climbs further.

Adds slightly to cost of maintenance (commission, spread) but is definitely much cheaper than buying pack a deflated option...

Am I missing something here??

Peter March 5th, 2012 at 5:51am

Well, I suppose that is the strategy ;-) short the put, wait for it to decline until you reach your profit target.

Newbz March 1st, 2012 at 7:10pm

Peter, yeah it would be a loss if I bought a short I sold at a higher price -- that makes sense.

Well, are there any strategies that involve writing a short contract for $1, hoping it goes down to 50cents then buying it back so you end up with a Net Gain of 50cents instead of the $1 premium?

Ideally, you want the option to expire, but maybe in the case of a naked call/put you'd buyback if you're worried about the buyer going through with the contract.

Peter March 1st, 2012 at 6:38pm

Hi Newbz, if you sell short a put at $1 and then buy the same put for $2 then you make a loss of $1. Just like you would if you bought it first for $2 and sold it out for $1.

But yes, the participant who holds the short position is the one who is ab ligated to deliver if assigned.

It might not necessarily be the same person who was on the other side of your transaction. The options clearing house aggregates all of the option positions based off the trading through a process called novation (see the section titled "Application in financial markets").

Newbz March 1st, 2012 at 4:56pm

Peter, it turns out there weren't any buyers for that option I was selling -- problem solved.

I have another question, and I asked a similar one to this in the Long Call entry on this site.

If I write a Short Put for $1 and lets say the value of that contract increases to $2 and now I want turn a profit. Is the person who buys the short put contract from me now obligated to fulfill the contract instead of me?

Peter March 1st, 2012 at 4:48pm

Hi Newbz, what is the simulator you are using?

I'm not sure how it all works with a simulator i.e. why there aren't any buyers or where the bids are supposed to come from...but if the option has some intrinsic value there will always be a buyer as market makers will bid basis getting a hedge in the underlying.

However, if the option is out-of-the-money and very close to expiration then it is possible that there won't be any buyers and you will just have to allow the option to expire worthless.

Newbz March 1st, 2012 at 10:59am

I'm using a stock simulator for short putting and I'm trying to sell 10 contracts of a 50cent strike price. The bid is 0 and the ask is 20cents.

Obviously selling it at 0 is pointless, so I tried 10cents and waited a bit...the order remained open. Moved it to 5cents and waited...still an open order.

I don't care about getting a sell price closer to the ask, but I don't want to settle on a bid of 0 either. This simulator only lets me increase the price in increments of 5cents, so I can't set my price to 1cent either.

This is only paper trading so it's not a big deal, but what happens if I encounter this problem during real trading. The contract will never get sold because it's not at bid price, which is 0 so why would I sell it.

Peter November 16th, 2011 at 7:46pm

Mmm..yeah, not too sure. I could guess and say that the $178 is the loss between the sold price and the current market price, however, you say 0.27 is the current price? Unless the position is valued against a price other than 0.27 - say average of the bid/ask spread or last, which may be some other price.

Then I would have said that the $280 was the loss including commissions. But that would suggest that you pay approximately $10 per contract in brokerage. What are your rates?

By the time the option expires, if it is still out-of-the-money, then the price of the option will have traded from 0.27 to zero so the unrealized losses will have been credited back into your account and you will be left with the $110 credit from the initial sale (minus brokerage fees).

Add a Comment