Option Portfolio

Market Close January 19, 2017

P&L up $3

| Symbol | Position | Price | Close | P&L |

|---|---|---|---|---|

| GLW Short Iron Condor | ||||

| GLW Feb17'17 $25 Call | -3 | 0.48 | 0.47 | 3 |

| GLW Feb17'17 $26 Call | 3 | 0.2 | 0.16 | -12 |

| GLW Feb17'17 $23 Put | -3 | 0.23 | 0.26 | -9 |

| GLW Feb17'17 $22 Put | 3 | 0.13 | 0.2 | 21 |

| Total | -1.14 | -1.11 | 3 | |

| Grand Total | 3 |

How to Adjust a Losing Iron Condor?

January 25th, 2017

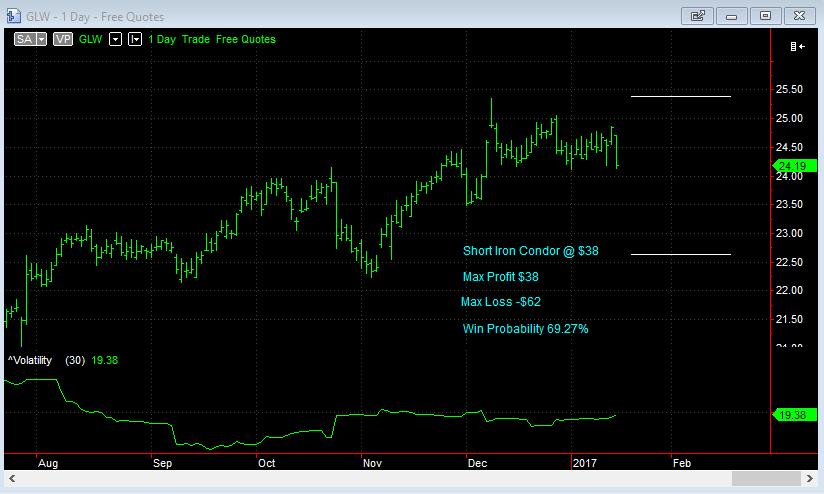

Looks like my pre-earnings Iron Condor strategy was indeed a bad idea. GLW released their earnings before the market opened Tuesday 24th January to the surprise of analysts.

Core EPS turned out to be $0.50 on a predicted $0.44. The stock opened strong and rallied higher throughout the day to close the session up 5.7% to $26.18.

The stock is now outside the upper breakeven point of $25.38 and if it continues I will realise my max loss of $186 ($62 per contract).

What Options do I have to Adjust?

I have a few alternatives to consider as to how to manage this trade at this point:

- Do nothing and hope that the market pulls back from now until expiration

- Sell a higher strike put spread

- Sell a higher strike put spread in the next expiration

- Reverse the existing short call spread into a long call spread

- Close the short call and leave the long call to run

- Double down with another Iron Condor

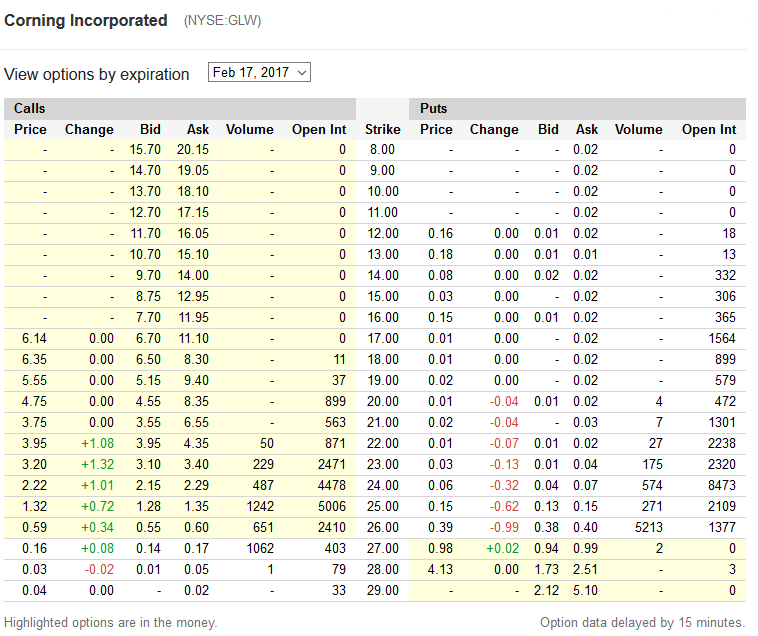

In considering the above, I looked at the option prices at the close for the Feb 17th options:

Since the pop in stock price due to earnings, the uncertainty has since been remove and can be seen in much lower option prices. Implied volatility has dropped to 18% so 2, 3 and 6 don’t look like bringing in much premium. Plus, putting on another Iron Condor in March would mean having to put it with narrow strikes in order to make it worthwhile but also means a lower chance of the stock staying between the bands.

Also to consider is the sentiment since the report, which was very favorable for the future outlook of the stock. I would say that I am now bullish on the stock.

Pre-market activity also shows a strong open with the stock having traded $26.30 with an hour before the open. So what I’m going to do is go with #5 above; close out the short $25 call and leave the $26 long call open. The $25 calls closed at $1.32 but with the pre-market looking to open higher, I’m not sure what price to go with. Perhaps yesterday’s offer price of $1.35?

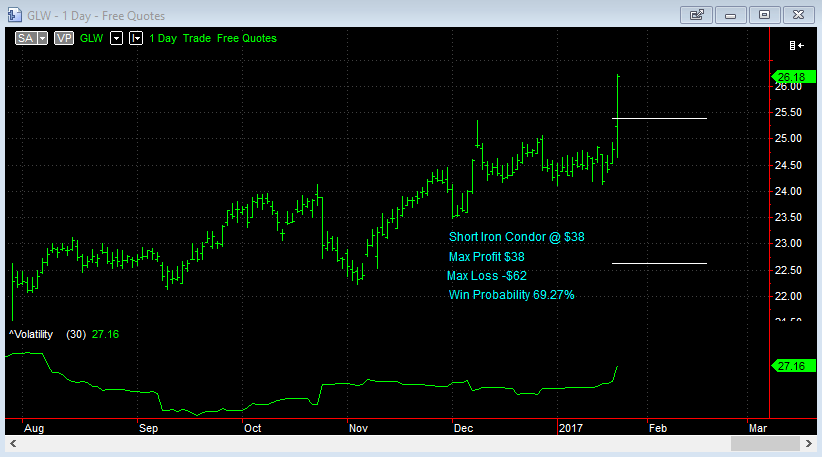

Iron Condor Pre-Earnings

January 19th, 2017

It's not always a good idea to take on short volatility strategies pre-earnings, but take a look at this Iron Condor setup for GLW.

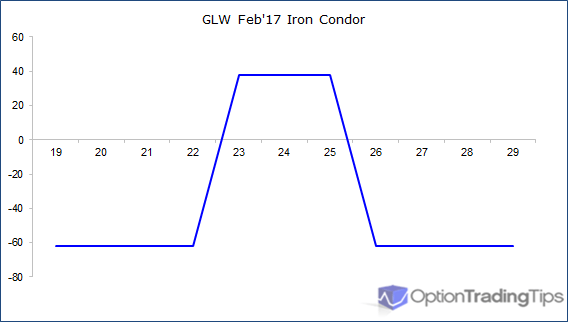

| B/S | Strike | C/P | Price |

|---|---|---|---|

| Sell | $25 | Call | 0.48 |

| Buy | $26 | Call | 0.20 |

| Sell | $23 | Put | 0.23 |

| Buy | $22 | Put | 0.13 |

| Total Credit | $38 | ||

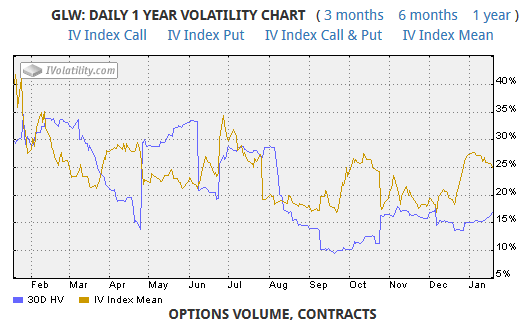

The stock has earnings out January 24th and the options expire February 17th. The implied volatility suggests there is some uncertainty leading into the announcement; IV is relatively high at 25% compared to historical vol of 15%.

Max profit on this is $38 per contract, which is the net credit received at the time of trade. Max loss is $62. At the current volatility level, there is a 69.27% chance of success with this trade.

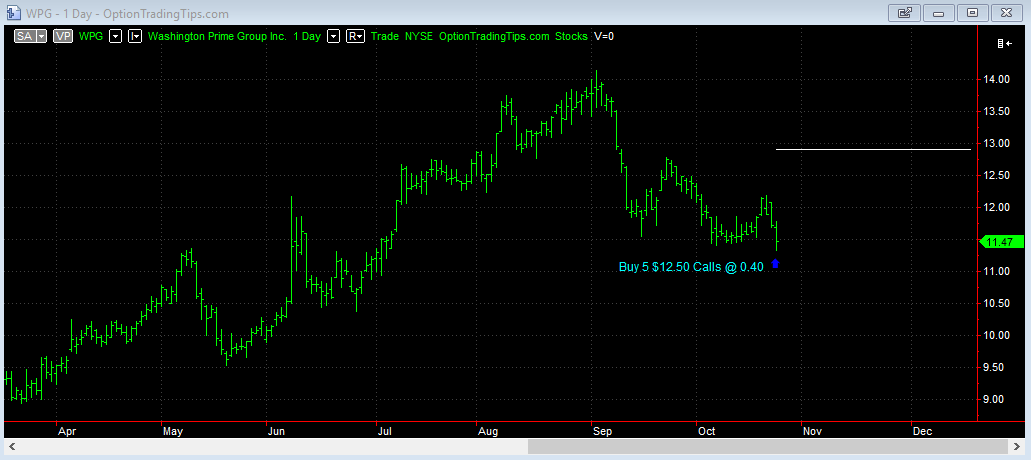

Long 5 $12.50 Call Options

Trade Start: 25th October

Description.

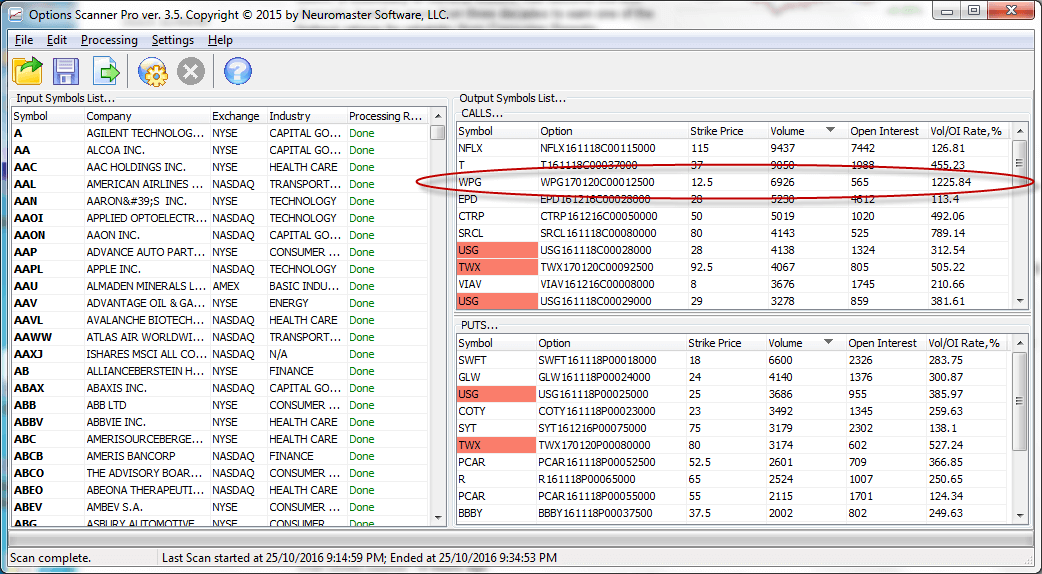

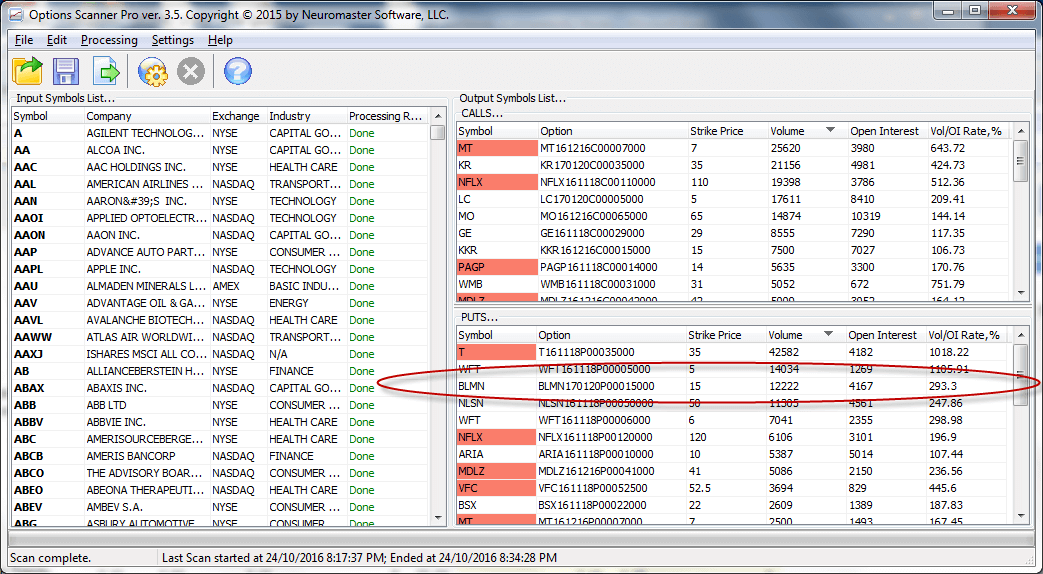

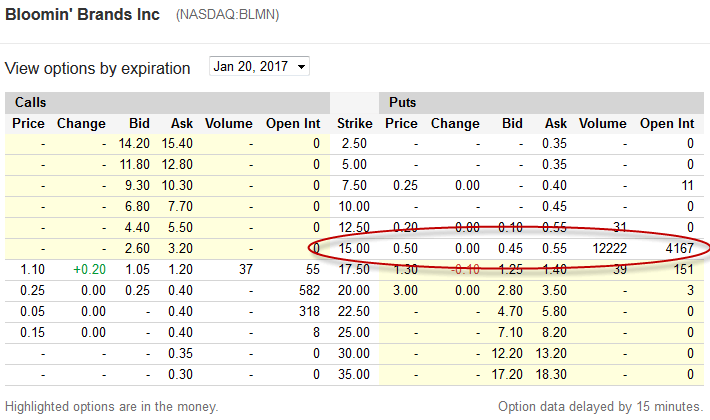

Option Scans for 24th October

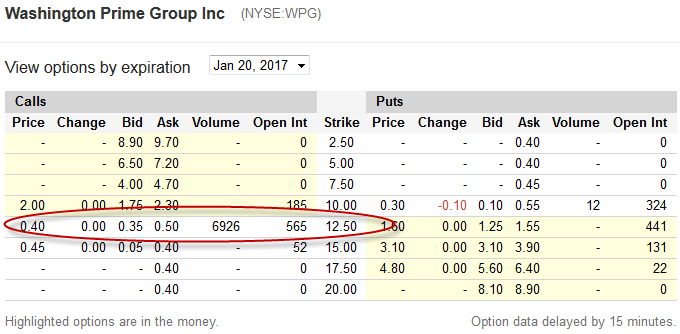

Option Prices for 24th October

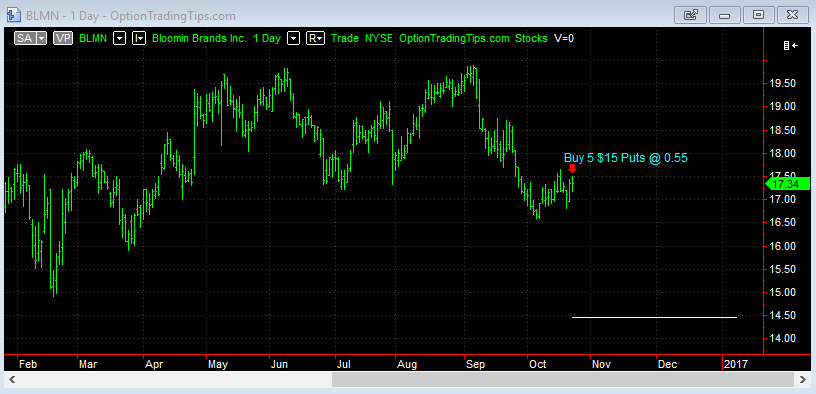

Long 5 $15 Put Options

Trade Start: 24th October, 2016

Only 0.55 for these puts when they are 3 months out. The chart doesn't make it look like a good trade but there's plenty of time in this one. Earnings are out October 28th.

Option Scans for 21st October

Option Prices for 21st October

2016 Closed Position Summary

| Trade | Open | Close | Days | P&L | Total |

|---|---|---|---|---|---|

| COH Iron Condor | 25-Jan-16 | 5-Feb-16 | 11 | 31.4 | 31.4 |

| COH Adj Call Spread | 3-Feb-16 | 5-Feb-16 | 2 | 55.5 | 86.9 |

| CAT Short Call Spread | 28-Jan-16 | 12-Feb-16 | 15 | -22.5 | 64.4 |

| COH Assignment | 8-Feb-16 | 12-Feb-16 | 4 | 74.6 | 139 |

| FCX Iron Butterfly | 28-Jan-16 | 18-Feb-16 | 21 | 35 | 174 |

| FSLR Iron Condor | 23-Feb-16 | 26-Feb-16 | 3 | -26.2 | 147.8 |

| TGT Short Call Spread | 23-Feb-16 | 26-Feb-16 | 3 | -66.6 | 81.2 |

| EPD Put Bear Spread | 29-Feb-16 | 18-Mar-16 | 18 | -40 | 41.2 |

| SPY Iron Condor | 2-Mar-16 | 4-Mar-16 | 2 | -22 | 19.2 |

| RCL Put Spread | 24-Mar-16 | 15-Apr-16 | 22 | -143.5 | -124.3 |

| MU Straddle | 30-Mar-16 | 1-Apr-16 | 2 | -50.6 | -174.9 |

| RIG Put Spread | 30-Mar-16 | 15-Apr-16 | 16 | -56.7 | -231.6 |

| VZ Long Call | 30-Mar-16 | 15-Apr-16 | 16 | -101.6 | -333.2 |

| JWN Long Put | 30-Mar-16 | 15-Apr-16 | 16 | 364.2 | 31 |

| C Straddle | 31-Mar-16 | 15-Apr-16 | 15 | 221.8 | 252.8 |

| EMC Long Put | 13-Apr-16 | 20-May-16 | 37 | -160 | 92.8 |

| ETE Long Call | 19-Apr-16 | 20-May-16 | 31 | 168 | 260.8 |

| MRO Long Call | 19-Apr-16 | 20-May-16 | 31 | -75 | 185.8 |

| KEY Long Call | 20-Apr-16 | 20-May-16 | 30 | 6 | 191.8 |

| MS Long Put | 20-Apr-16 | 20-May-16 | 30 | -100 | 91.8 |

| VALE Long Put | 21-Apr-16 | 20-May-16 | 29 | 360 | 451.8 |

| JNPR Long Put | 21-Apr-16 | 20-May-16 | 29 | -62 | 389.8 |

| KMI Long Call | 28-Apr-16 | 20-May-16 | 22 | -100 | 289.8 |

| IPHI Long Call | 29-Apr-16 | 20-May-16 | 21 | -55 | 234.8 |

| NG Long Call | 29-Apr-16 | 20-May-16 | 21 | -80 | 154.8 |

| MRO Short Call | 29-Apr-16 | 20-May-16 | 21 | 55 | 209.8 |

| CTL Long Put | 2-May-16 | 20-May-16 | 18 | 212 | 421.8 |

| HIMX Long Call | 9-May-16 | 13-May-16 | 4 | -55 | 366.8 |

| ETE Short Call | 10-May-16 | 20-May-16 | 10 | 55 | 421.8 |

| VIAV Long Call | 24-May-16 | 17-Jun-16 | 24 | -100 | 321.8 |

| CYH Long Strangle | 25-May-16 | 17-Jun-16 | 23 | -110 | 211.8 |

| HBI Long Strangle | 31-May-16 | 17-Jun-16 | 17 | -115 | 96.8 |

| ANF Long Put | 31-May-16 | 17-Jun-16 | 17 | -90 | 6.8 |

| RF Long Call | 1-Jun-16 | 17-Jun-16 | 16 | -80 | -73.2 |

| WLL Long Put | 8-Jun-16 | 24-Jun-16 | 16 | 300 | 226.8 |

| ANF Covered Put | 17-Jun-16 | 24-Jun-16 | 7 | 60 | 286.8 |

| ATVI Put Spread | 2-Jun-16 | 15-Jul-16 | 43 | -126 | 160.8 |

| CY Long Call | 2-Jun-16 | 15-Jul-16 | 43 | -42 | 118.8 |

| GOGO Long Put | 6-Jun-16 | 15-Jul-16 | 39 | -124 | -5.2 |

| VLO Long Put | 6-Jun-16 | 15-Jul-16 | 39 | -100 | -105.2 |

| RBS Long Call | 8-Jun-16 | 15-Jul-16 | 37 | -120 | -225.2 |

| PBI Long Call | 9-Jun-16 | 15-Jul-16 | 36 | -100 | -325.2 |

| GGAL Long Call | 9-Jun-16 | 15-Jul-16 | 36 | 60 | -265.2 |

| MT Long Call | 9-Jun-16 | 15-Jul-16 | 36 | -110 | -375.2 |

| PLD Long Call | 9-Jun-16 | 15-Jul-16 | 36 | 90 | -285.2 |

| VIAV Covered Call | 22-Jun-16 | 22-Jul-16 | 30 | 258 | -27.2 |

| BID Long Call | 11-Jul-16 | 9-Aug-16 | 29 | 1950 | 1922.8 |

| NLY Long Put | 8-Jul-16 | 19-Aug-16 | 42 | -90 | 1832.8 |

| LGF Long Put | 8-Jul-16 | 19-Aug-16 | 42 | -145 | 1687.8 |

| CMCSA Long Call | 11-Jul-16 | 19-Aug-16 | 39 | -100 | 1587.8 |

| D Long Put | 26-Jul-16 | 19-Aug-16 | 24 | -135 | 1452.8 |

| PEG Long Put | 27-Jul-16 | 19-Aug-16 | 23 | 140 | 1592.8 |

| KR Long Call | 27-Jul-16 | 19-Aug-16 | 23 | -150 | 1442.8 |

| DB Long Put | 11-Aug-16 | 16-Sep-16 | 36 | -150 | 1292.8 |

| LOW Long Put | 11-Aug-16 | 16-Sep-16 | 36 | 1050 | 2342.8 |

| FIT Long Call | 11-Aug-16 | 16-Sep-16 | 36 | -126 | 2216.8 |

| GT Long Call | 18-Aug-16 | 16-Sep-16 | 29 | 450 | 2666.8 |

| NUAN Long Put | 18-Aug-16 | 16-Sep-16 | 29 | -140 | 2526.8 |

| GFI Long Call | 13-Sep-16 | 21-Oct-16 | 38 | -170 | 2356.8 |

| EGO Long Call | 14-Sep-16 | 21-Oct-16 | 37 | -200 | 2156.8 |

| CCL Long Put | 19-Sep-16 | 21-Oct-16 | 32 | -120 | 2036.8 |

| BAC Long Butterfly | 27-Sep-16 | 21-Oct-16 | 24 | 105 | 2022.8 |

| DDD Long Put | 20-Sep-16 | 27-Oct-16 | 37 | -49 | 1987.8 |

| JCP Long Call Spread | 23-Sep-16 | 27-Oct-16 | 34 | -47 | 1940.8 |

| CNP Long Call | 26-Sep-16 | 27-Oct-16 | 31 | -150 | 1790.8 |

2015 Closed Position Summary

| Trade | Open | Close | Days | P&L | Total |

|---|---|---|---|---|---|

| BBY Short Put | 6-Jan-15 | 17-Jan-15 | 11 | 69 | 69 |

| F Long Call | 9-Jan-15 | 30-Jan-15 | 21 | -20 | 49 |

| AVP Calendar | 14-Jan-15 | 27-Feb-15 | 44 | -23 | 26 |

| AVP Put Spread | 14-Jan-15 | 27-Feb-15 | 44 | -32 | -6 |

| COH Short Condor | 15-Jan-15 | 30-Jan-15 | 15 | 81 | 75 |

| GRPN Buy-Write | 23-Jan-15 | 13-Feb-15 | 21 | -36 | 39 |

| WTW Short Put | 23-Jan-15 | 2-Mar-15 | 38 | -560 | -521 |

| CRUS Double Calendar | 26-Jan-15 | 30-Jan-15 | 4 | -1 | -522 |

| SPY Short Condor | 12-Feb-15 | 20-Feb-15 | 8 | -66.4 | -588.4 |

| MX Double Calendar | 13-Feb-15 | 20-Mar-15 | 35 | -71.6 | -660 |

| JCP Double Calendar | 25-Feb-15 | 13-Mar-15 | 16 | -3 | -663 |

| KYTH Short Butterfly | 25-Feb-15 | 20-Mar-15 | 23 | -100 | -763 |

| TASR Short Condor | 25-Feb-15 | 20-Mar-15 | 23 | 35 | -728 |

| BBRY Long Butterfly | 24-Mar-15 | 2-Apr-15 | 9 | -84 | -812 |

| BTU Long Put Spread | 12-Jun-15 | 3-Jul-15 | 21 | 117.5 | -694.5 |

| MU Long Put Spread | 17-Jun-15 | 3-Jul-15 | 16 | 71.4 | -623.1 |

| RAD Short Call Spread | 19-Jun-15 | 3-Jul-15 | 14 | 92 | -531.1 |

49 Comments

Ratha August 27th, 2013 at 9:14pm

Hi Peter

Many thanks for your replying to me quickly.

But what i would like to do in this case is that i don't understand how to calculate general market risk of equity option risk under scenario approach in market risk as in example linked : http://www.bnm.gov.my/guidelines/01_banking/01_capital_adequacy/gl_05_Capital_adequacy_framework_RWA.pdf

in page 298 described about General Risk to Scenario Approach in b) and c) which shows the result -15.57, -9.21, -0.92.....how to calculate it?

Best Wishes

Peter August 26th, 2013 at 6:15pm

Hi Ratha,

You're welcome to put together your own using my options pricing spreadsheet as a base - or you can use an online version of the option calculator.

Ratha August 25th, 2013 at 11:52pm

Hi sir

I would like to all of you to explain me how to calculate the matrix in call or put option. price interval 8%, volatility 15%, market value $19.09, strike price $20, risk-free rate 5%, residual maturity 0.36 year, annual dividend rate 0%.

Thanks for your respond.

Peter August 1st, 2013 at 6:40pm

Hi Greg, Which spreadsheet are you having troubles with: the pricing or the volatility spreadsheet? Have you seen the support page?

Greg August 1st, 2013 at 1:53pm

I tried using the workbook spreadsheet but not sure if I am using it correctly. Are there direction or phone # I can call for help???

Peter February 4th, 2013 at 4:11pm

Hi Vidur,

Long straddles are good strategy when you expect a large move in the underlying, however, the movement needed for the strategy to be profitable depends on the length of time until the expiration of the options and the total price of the straddle.

For example, the straddle may be priced so high that the stock may need to move 4% just to break even. Alternatively, if the implied volatility is low a 2 to 3% move may just result in a decent profit.

vidur gupta February 4th, 2013 at 9:49am

first of all thanks for the insights .. really appreciate it !!

Is long strangle a good strategy to be played when you expect 2-3% move in stock ??

Optionsbear January 19th, 2013 at 3:20pm

Hello what do you know about Second order greeks vanna, vomma?

Arun December 25th, 2012 at 3:42am

Very Nice....

Peter August 29th, 2012 at 10:53pm

Mmm - you're right. The data comes from Yahoo and they seem to be behind on the latest data for India. I'm not sure when NSE data is updated to Yahoo - hopefully before the market opens!

Add a Comment