Option Portfolio

Market Close January 19, 2017

P&L up $3

| Symbol | Position | Price | Close | P&L |

|---|---|---|---|---|

| GLW Short Iron Condor | ||||

| GLW Feb17'17 $25 Call | -3 | 0.48 | 0.47 | 3 |

| GLW Feb17'17 $26 Call | 3 | 0.2 | 0.16 | -12 |

| GLW Feb17'17 $23 Put | -3 | 0.23 | 0.26 | -9 |

| GLW Feb17'17 $22 Put | 3 | 0.13 | 0.2 | 21 |

| Total | -1.14 | -1.11 | 3 | |

| Grand Total | 3 |

How to Adjust a Losing Iron Condor?

January 25th, 2017

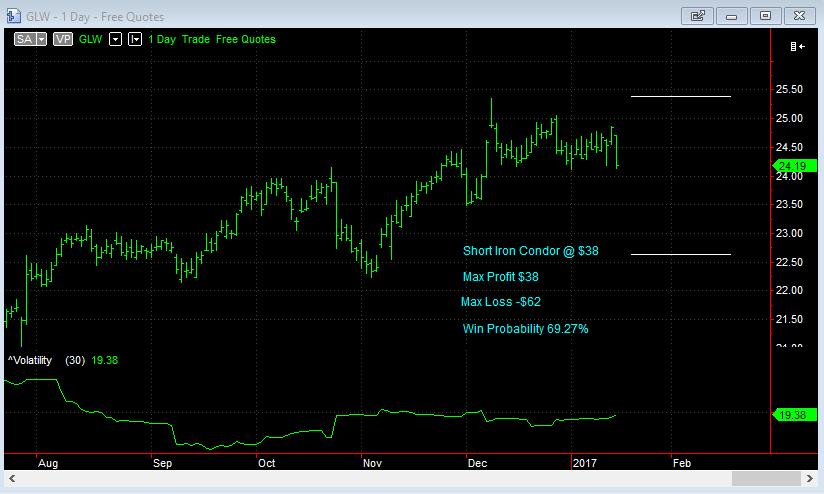

Looks like my pre-earnings Iron Condor strategy was indeed a bad idea. GLW released their earnings before the market opened Tuesday 24th January to the surprise of analysts.

Core EPS turned out to be $0.50 on a predicted $0.44. The stock opened strong and rallied higher throughout the day to close the session up 5.7% to $26.18.

The stock is now outside the upper breakeven point of $25.38 and if it continues I will realise my max loss of $186 ($62 per contract).

What Options do I have to Adjust?

I have a few alternatives to consider as to how to manage this trade at this point:

- Do nothing and hope that the market pulls back from now until expiration

- Sell a higher strike put spread

- Sell a higher strike put spread in the next expiration

- Reverse the existing short call spread into a long call spread

- Close the short call and leave the long call to run

- Double down with another Iron Condor

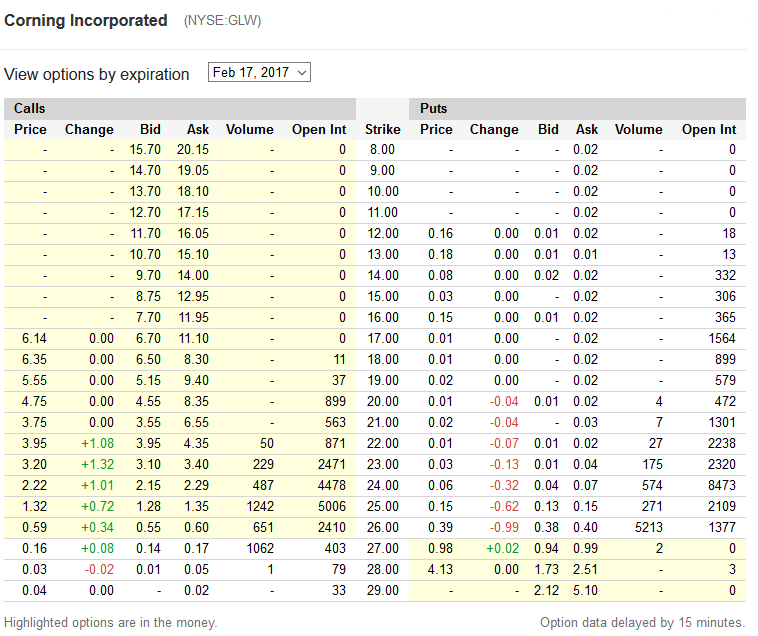

In considering the above, I looked at the option prices at the close for the Feb 17th options:

Since the pop in stock price due to earnings, the uncertainty has since been remove and can be seen in much lower option prices. Implied volatility has dropped to 18% so 2, 3 and 6 don’t look like bringing in much premium. Plus, putting on another Iron Condor in March would mean having to put it with narrow strikes in order to make it worthwhile but also means a lower chance of the stock staying between the bands.

Also to consider is the sentiment since the report, which was very favorable for the future outlook of the stock. I would say that I am now bullish on the stock.

Pre-market activity also shows a strong open with the stock having traded $26.30 with an hour before the open. So what I’m going to do is go with #5 above; close out the short $25 call and leave the $26 long call open. The $25 calls closed at $1.32 but with the pre-market looking to open higher, I’m not sure what price to go with. Perhaps yesterday’s offer price of $1.35?

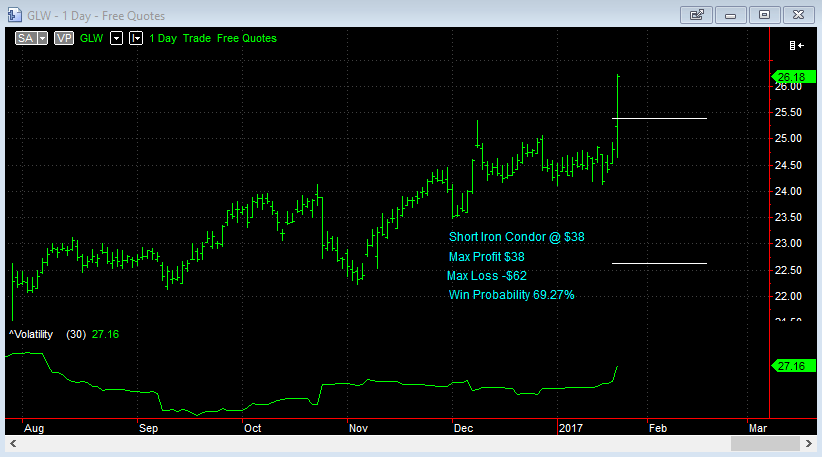

Iron Condor Pre-Earnings

January 19th, 2017

It's not always a good idea to take on short volatility strategies pre-earnings, but take a look at this Iron Condor setup for GLW.

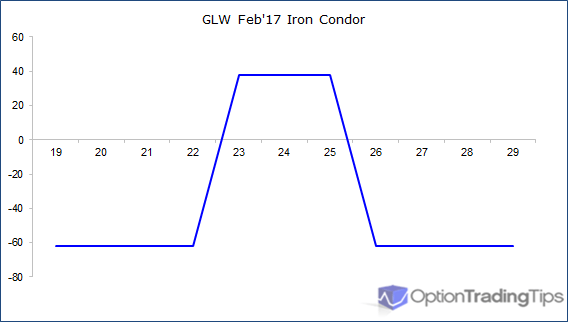

| B/S | Strike | C/P | Price |

|---|---|---|---|

| Sell | $25 | Call | 0.48 |

| Buy | $26 | Call | 0.20 |

| Sell | $23 | Put | 0.23 |

| Buy | $22 | Put | 0.13 |

| Total Credit | $38 | ||

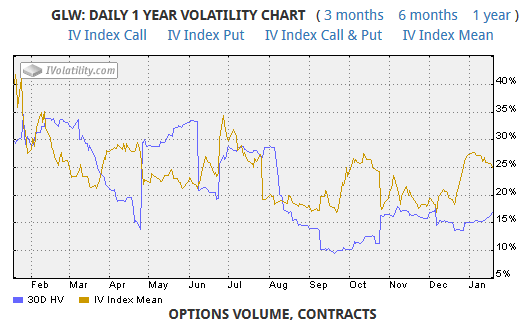

The stock has earnings out January 24th and the options expire February 17th. The implied volatility suggests there is some uncertainty leading into the announcement; IV is relatively high at 25% compared to historical vol of 15%.

Max profit on this is $38 per contract, which is the net credit received at the time of trade. Max loss is $62. At the current volatility level, there is a 69.27% chance of success with this trade.

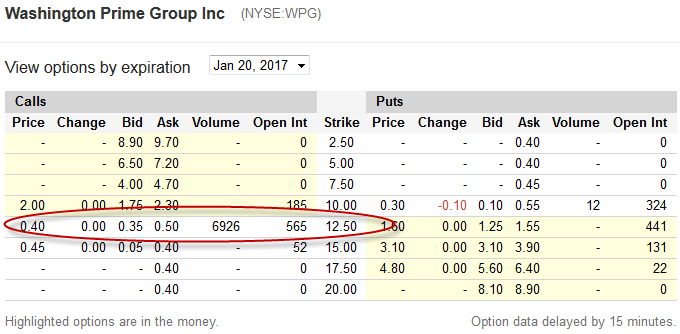

Long 5 $12.50 Call Options

Trade Start: 25th October

Description.

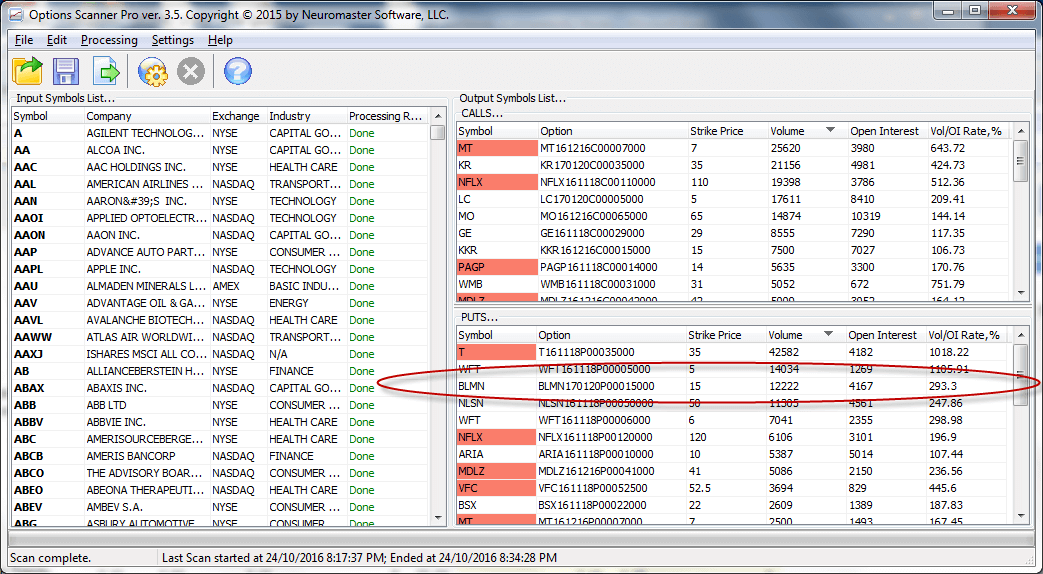

Option Scans for 24th October

Option Prices for 24th October

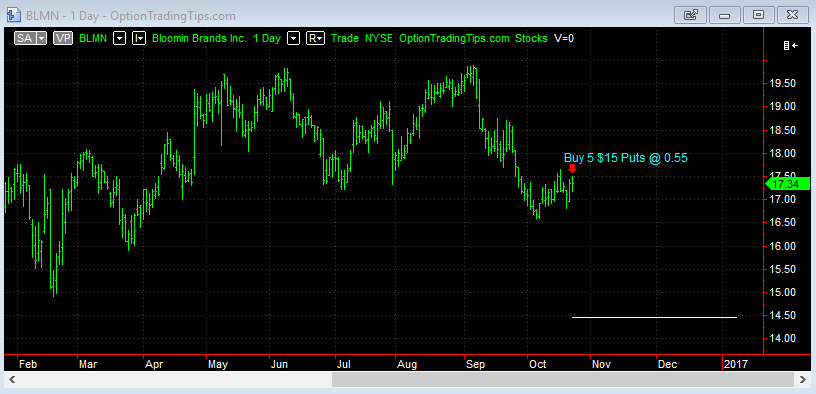

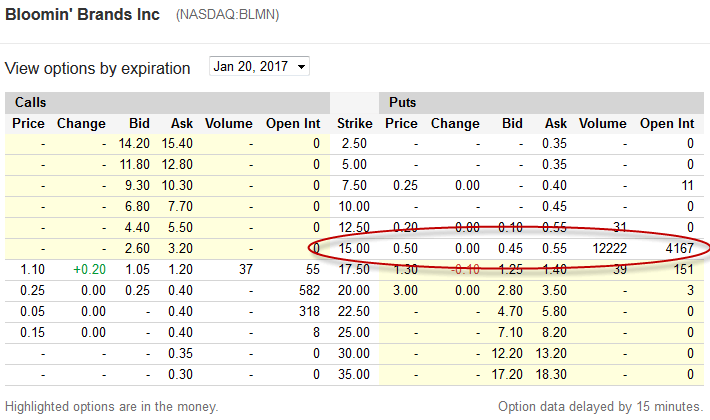

Long 5 $15 Put Options

Trade Start: 24th October, 2016

Only 0.55 for these puts when they are 3 months out. The chart doesn't make it look like a good trade but there's plenty of time in this one. Earnings are out October 28th.

Option Scans for 21st October

Option Prices for 21st October

2016 Closed Position Summary

| Trade | Open | Close | Days | P&L | Total |

|---|---|---|---|---|---|

| COH Iron Condor | 25-Jan-16 | 5-Feb-16 | 11 | 31.4 | 31.4 |

| COH Adj Call Spread | 3-Feb-16 | 5-Feb-16 | 2 | 55.5 | 86.9 |

| CAT Short Call Spread | 28-Jan-16 | 12-Feb-16 | 15 | -22.5 | 64.4 |

| COH Assignment | 8-Feb-16 | 12-Feb-16 | 4 | 74.6 | 139 |

| FCX Iron Butterfly | 28-Jan-16 | 18-Feb-16 | 21 | 35 | 174 |

| FSLR Iron Condor | 23-Feb-16 | 26-Feb-16 | 3 | -26.2 | 147.8 |

| TGT Short Call Spread | 23-Feb-16 | 26-Feb-16 | 3 | -66.6 | 81.2 |

| EPD Put Bear Spread | 29-Feb-16 | 18-Mar-16 | 18 | -40 | 41.2 |

| SPY Iron Condor | 2-Mar-16 | 4-Mar-16 | 2 | -22 | 19.2 |

| RCL Put Spread | 24-Mar-16 | 15-Apr-16 | 22 | -143.5 | -124.3 |

| MU Straddle | 30-Mar-16 | 1-Apr-16 | 2 | -50.6 | -174.9 |

| RIG Put Spread | 30-Mar-16 | 15-Apr-16 | 16 | -56.7 | -231.6 |

| VZ Long Call | 30-Mar-16 | 15-Apr-16 | 16 | -101.6 | -333.2 |

| JWN Long Put | 30-Mar-16 | 15-Apr-16 | 16 | 364.2 | 31 |

| C Straddle | 31-Mar-16 | 15-Apr-16 | 15 | 221.8 | 252.8 |

| EMC Long Put | 13-Apr-16 | 20-May-16 | 37 | -160 | 92.8 |

| ETE Long Call | 19-Apr-16 | 20-May-16 | 31 | 168 | 260.8 |

| MRO Long Call | 19-Apr-16 | 20-May-16 | 31 | -75 | 185.8 |

| KEY Long Call | 20-Apr-16 | 20-May-16 | 30 | 6 | 191.8 |

| MS Long Put | 20-Apr-16 | 20-May-16 | 30 | -100 | 91.8 |

| VALE Long Put | 21-Apr-16 | 20-May-16 | 29 | 360 | 451.8 |

| JNPR Long Put | 21-Apr-16 | 20-May-16 | 29 | -62 | 389.8 |

| KMI Long Call | 28-Apr-16 | 20-May-16 | 22 | -100 | 289.8 |

| IPHI Long Call | 29-Apr-16 | 20-May-16 | 21 | -55 | 234.8 |

| NG Long Call | 29-Apr-16 | 20-May-16 | 21 | -80 | 154.8 |

| MRO Short Call | 29-Apr-16 | 20-May-16 | 21 | 55 | 209.8 |

| CTL Long Put | 2-May-16 | 20-May-16 | 18 | 212 | 421.8 |

| HIMX Long Call | 9-May-16 | 13-May-16 | 4 | -55 | 366.8 |

| ETE Short Call | 10-May-16 | 20-May-16 | 10 | 55 | 421.8 |

| VIAV Long Call | 24-May-16 | 17-Jun-16 | 24 | -100 | 321.8 |

| CYH Long Strangle | 25-May-16 | 17-Jun-16 | 23 | -110 | 211.8 |

| HBI Long Strangle | 31-May-16 | 17-Jun-16 | 17 | -115 | 96.8 |

| ANF Long Put | 31-May-16 | 17-Jun-16 | 17 | -90 | 6.8 |

| RF Long Call | 1-Jun-16 | 17-Jun-16 | 16 | -80 | -73.2 |

| WLL Long Put | 8-Jun-16 | 24-Jun-16 | 16 | 300 | 226.8 |

| ANF Covered Put | 17-Jun-16 | 24-Jun-16 | 7 | 60 | 286.8 |

| ATVI Put Spread | 2-Jun-16 | 15-Jul-16 | 43 | -126 | 160.8 |

| CY Long Call | 2-Jun-16 | 15-Jul-16 | 43 | -42 | 118.8 |

| GOGO Long Put | 6-Jun-16 | 15-Jul-16 | 39 | -124 | -5.2 |

| VLO Long Put | 6-Jun-16 | 15-Jul-16 | 39 | -100 | -105.2 |

| RBS Long Call | 8-Jun-16 | 15-Jul-16 | 37 | -120 | -225.2 |

| PBI Long Call | 9-Jun-16 | 15-Jul-16 | 36 | -100 | -325.2 |

| GGAL Long Call | 9-Jun-16 | 15-Jul-16 | 36 | 60 | -265.2 |

| MT Long Call | 9-Jun-16 | 15-Jul-16 | 36 | -110 | -375.2 |

| PLD Long Call | 9-Jun-16 | 15-Jul-16 | 36 | 90 | -285.2 |

| VIAV Covered Call | 22-Jun-16 | 22-Jul-16 | 30 | 258 | -27.2 |

| BID Long Call | 11-Jul-16 | 9-Aug-16 | 29 | 1950 | 1922.8 |

| NLY Long Put | 8-Jul-16 | 19-Aug-16 | 42 | -90 | 1832.8 |

| LGF Long Put | 8-Jul-16 | 19-Aug-16 | 42 | -145 | 1687.8 |

| CMCSA Long Call | 11-Jul-16 | 19-Aug-16 | 39 | -100 | 1587.8 |

| D Long Put | 26-Jul-16 | 19-Aug-16 | 24 | -135 | 1452.8 |

| PEG Long Put | 27-Jul-16 | 19-Aug-16 | 23 | 140 | 1592.8 |

| KR Long Call | 27-Jul-16 | 19-Aug-16 | 23 | -150 | 1442.8 |

| DB Long Put | 11-Aug-16 | 16-Sep-16 | 36 | -150 | 1292.8 |

| LOW Long Put | 11-Aug-16 | 16-Sep-16 | 36 | 1050 | 2342.8 |

| FIT Long Call | 11-Aug-16 | 16-Sep-16 | 36 | -126 | 2216.8 |

| GT Long Call | 18-Aug-16 | 16-Sep-16 | 29 | 450 | 2666.8 |

| NUAN Long Put | 18-Aug-16 | 16-Sep-16 | 29 | -140 | 2526.8 |

| GFI Long Call | 13-Sep-16 | 21-Oct-16 | 38 | -170 | 2356.8 |

| EGO Long Call | 14-Sep-16 | 21-Oct-16 | 37 | -200 | 2156.8 |

| CCL Long Put | 19-Sep-16 | 21-Oct-16 | 32 | -120 | 2036.8 |

| BAC Long Butterfly | 27-Sep-16 | 21-Oct-16 | 24 | 105 | 2022.8 |

| DDD Long Put | 20-Sep-16 | 27-Oct-16 | 37 | -49 | 1987.8 |

| JCP Long Call Spread | 23-Sep-16 | 27-Oct-16 | 34 | -47 | 1940.8 |

| CNP Long Call | 26-Sep-16 | 27-Oct-16 | 31 | -150 | 1790.8 |

2015 Closed Position Summary

| Trade | Open | Close | Days | P&L | Total |

|---|---|---|---|---|---|

| BBY Short Put | 6-Jan-15 | 17-Jan-15 | 11 | 69 | 69 |

| F Long Call | 9-Jan-15 | 30-Jan-15 | 21 | -20 | 49 |

| AVP Calendar | 14-Jan-15 | 27-Feb-15 | 44 | -23 | 26 |

| AVP Put Spread | 14-Jan-15 | 27-Feb-15 | 44 | -32 | -6 |

| COH Short Condor | 15-Jan-15 | 30-Jan-15 | 15 | 81 | 75 |

| GRPN Buy-Write | 23-Jan-15 | 13-Feb-15 | 21 | -36 | 39 |

| WTW Short Put | 23-Jan-15 | 2-Mar-15 | 38 | -560 | -521 |

| CRUS Double Calendar | 26-Jan-15 | 30-Jan-15 | 4 | -1 | -522 |

| SPY Short Condor | 12-Feb-15 | 20-Feb-15 | 8 | -66.4 | -588.4 |

| MX Double Calendar | 13-Feb-15 | 20-Mar-15 | 35 | -71.6 | -660 |

| JCP Double Calendar | 25-Feb-15 | 13-Mar-15 | 16 | -3 | -663 |

| KYTH Short Butterfly | 25-Feb-15 | 20-Mar-15 | 23 | -100 | -763 |

| TASR Short Condor | 25-Feb-15 | 20-Mar-15 | 23 | 35 | -728 |

| BBRY Long Butterfly | 24-Mar-15 | 2-Apr-15 | 9 | -84 | -812 |

| BTU Long Put Spread | 12-Jun-15 | 3-Jul-15 | 21 | 117.5 | -694.5 |

| MU Long Put Spread | 17-Jun-15 | 3-Jul-15 | 16 | 71.4 | -623.1 |

| RAD Short Call Spread | 19-Jun-15 | 3-Jul-15 | 14 | 92 | -531.1 |

49 Comments

allan April 19th, 2012 at 10:40am

I sent a reply but dont see it listed but I did see this comment from u in answer to another comment-"At the expiration date, the option will be worth the intrinsic value, which will be the stock price minus the strike price.

In my example-my strike was 440 and at expiration the common price was flat at 608.34-so this is my understanding 608.34-440=168.34x100=$16,834 which is the amount of my prem cost-

My question is why is my option worthless-I dont understand? thx-

allan April 19th, 2012 at 10:01am

I dont understand -doesnt my strike price of $440 vs common price at expiration of 608.34 have any value?

Peter April 18th, 2012 at 10:58pm

Hi Allan,

If the option price is 168.03 then the premium you pay will be 16,803. You pay this at the time of the trade so it is essentially "lost" on the trade date.

You only make money if the value of the option increase in price from where it was purchased. So when you sell it the money received is more than what was paid out, which will be your profit.

Hope that makes sense.

allan April 18th, 2012 at 9:56pm

I just stumbled on this site-great info about options. My question concerns the purchase of a deep in the money call option at a strike price below the price of the common. ie Share price of appl today is 608.34-I want to buy an appl call- strike price- 440-prem 168.03- total cost 608.03. On expiration if the appl share price is above my 440 strike price will I lose my premium?

Peter April 9th, 2012 at 5:49pm

Hi Inderjit,

I recommend the example from Willow Solutions for this.

inderjit April 6th, 2012 at 3:30pm

Hi Peter - I downloaded your stock volatility spreadsheet and wanted to have a look at the VBA but this is password protected. I work with databases and wanted to see how you can connect to a web server and extract the data. Would really appreciate if you can let me have a look at the code. Thanks for your site.

Dharmendra February 26th, 2012 at 11:55am

Hi Peter.

I trade futures in commodities. I want to learn options in Gold, Crude and S&P. Can you help me out for the same ?

Dharmendra Bhagat

Mobile :+971508980047

email : [email protected]

skype : tridentjewels

Twitter : dharamjee

benila anoop February 21st, 2012 at 1:04am

hai peter,

i would like to start trading.. What should i do? Can you help me sir.

Peter August 28th, 2011 at 5:33pm

You mean you want to start trading the VIX?

Manish kumar August 28th, 2011 at 10:10am

Hi, I'm an option trader nifty index only I want to say thanks lot because I learn lot of thing from your option trading workbook, and now I want to improve my trading style at high and low VIX. How i improve myself advice me?

Add a Comment